If the public cloud computing market were our solar system, then Amazon Web Services would be Jupiter and Saturn together and the remaining five fast-growing big clouds would be like the inner planets like Mercury, Venus, Earth, Mars, and that pile of rocks that used to be a planet mixed up with those clouds that are finding growth a bit more challenging – think Uranus and Neptune and maybe even Pluto if you still want to count it a planet.

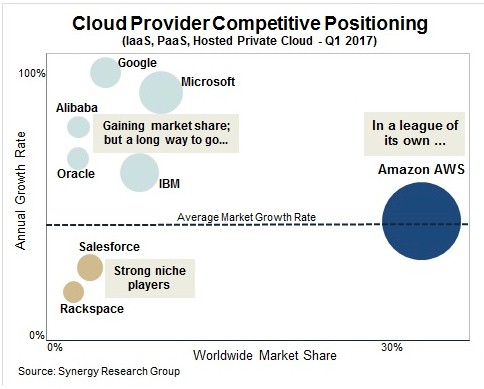

This analogy came to us in the wake of Amazon’s reporting of its financial results for the first quarter of 2017 last week and reviewing the cloud computing comparisons that are put together by Synergy Research. This chart certainly evokes that image:

The thing to remember about the planets is that even though Jupiter is certainly huge at 1,898 x 1024 kilograms (or 1.89 trillion trillion metric tons), and Saturn weighs in at 569 x 1024 kilograms, or about a third of the mass, and the Sun is a whopper at 1,989 x 1027 kilograms and that is over three orders of magnitude more mass. In this analogy, AWS, which is by far the largest of the public cloud suppliers, is still far smaller than the aggregate IT market, which comes to about $2 trillion for hardware, software, and services and over $3 trillion if you add in the telecom bills for corporations.

As far as Synergy Research can tell, AWS has managed to hold its share of the market steady at 33 percent, which is a feat for such a relative newcomer to the IT sector. The cloud business – meaning raw infrastructure services and higher level platform services as well as hosted private cloud offerings – hit nearly $10 billion across the globe in the first quarter, more than 40 percent higher than a year ago. Software as a service, or SaaS, is not counted as cloud in these numbers, and IBM, Oracle, and Salesforce have quite large businesses in this area.

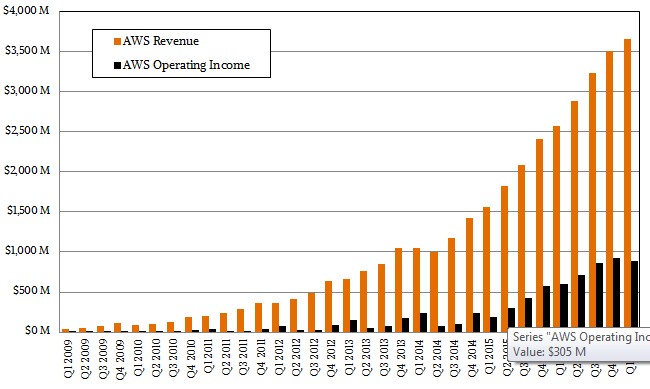

The math on that raw cloud market is not quite right there, but the way, and it is not our fault. AWS had $3.66 billion in sales in the first quarter, up 42.7 percent from the year ago period, and if it had a 33 percent share, that would make the overall market worth $11.1 billion. So either the AWS share is higher than 33 percent, the market is larger than Synergy Research’s statement says, or some mix of the two.

At this point, Google Cloud Platform is growing faster than Microsoft Azure, but it is still smaller; IBM is somewhere in between Google and Microsoft in terms of revenue, but it is mostly peddling hosted private cloud, which if you use Amazon’s definition of cloud is not cloud at all but just gussied up hosting. Oracle, by virtual of its 400,000-strongh customer base, has been able to ramp up a cloud business fairly quickly, just like Microsoft was able to do once it really started pushing Azure and, specifically, the kinds of adjunct services that existing customers could easily adopt.

The AWS revenue growth curve is the envy of the world, and has continued its acceleration even after a slight lull after a massive price cut on various infrastructure services in late 2013. The growth at AWS has not slowed as much now as it did back then, but it is not clear that the higher level platform services as well as an increasing appetite for capacity among its existing customers plus the budgets from new customers will be enough to get growth that is in the zone of 80 percent again. It is hard to keep chopping prices and growing a business by improving customer services at the same time, but this is what Amazon, the online retailer, does brilliantly. And there were seven price decreases on AWS that took effect December 1 last year that impacted the top and bottom line for AWS in the first quarter. Also, more customers are moving to Reserved Instances, which is why Amazon’s deferred revenue cash pile is growing. (The Amazon Prime delivery fee, which is allocated over time, is also boosting deferred revenue.)

Despite all of this downward pressure, AWS is getting better at squeezing more money out of its operations, and operating income grew slightly faster than revenue, at 47.4 percent in the first quarter, to hit $890 million. In the trailing twelve months, AWS has raked in $13.3 billion and it has brought $3.4 billion of that, or 25.6 percent, to the middle line. With the overall Amazon business only posting a net income of $724 million in the quarter, it is safe to say that without AWS, Amazon would not be a profitable business at all, and would not have been so for the past several years. And Jeff Bezos would not have been able to indulge in content and device creation on the scale he has enjoyed for his company. (Yeah, shareholders own Amazon, but founders never act like it.)

We think it is safe to assume that others will have a hard time competing on price and service, excepting the very largest competitors, like Google and Microsoft who have hyperscale, and niche players like Rackspace Hosting, IBM, and Oracle, who can play to their bases like Microsoft has so well. With tens of millions of enterprise customers worldwide, Microsoft has the largest potential customer base of them all, and it is always important to remember that.

But AWS will get its share, too. For instance, in the conference call with Wall Street analysts going over the Q1 2017 numbers, Amazon chief financial officer Brian Olsavsky said that more than 23,000 databases had been ported to its AWS cloud using the Database Migration Service, which launched last March. This sounds like a lot, and it is if Olsavsky meant to say database management systems, but if he really meant databases, then this is a drop in the bucket since enterprises have thousands to tens of thousands of applications, most of them driven by distinct databases.

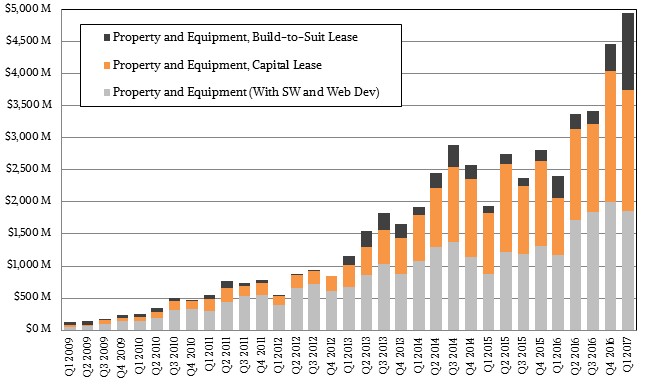

The interesting thing to note about the most recent numbers out of parent company Amazon is that it did a massive investment spike in property and equipment in the first quarter, with an unusually large jump in build-to-suit leases. The first quarters of 2015 and 2016 were pretty weak ones, but not so for 2017, and we think that AWS has been getting truckloads of “Skylake” Xeon systems in the past three months ahead of Intel’s formal launch of the chips sometime around the middle of the year. (We think July is looking likely.) Of course, Amazon builds a lot of other infrastructure, including warehouses for its retail business, so it is unclear how much of this spike is due to datacenter buildouts and system upgrades.

At over a $14 billion annualized run rate, AWS has built one of the most intricate, elegant, and successful platforms in the history of enterprise computing. It really does rival the IBM System/360 mainframe from five decades ago in terms of its scope and effect on shaping the whole nature of data processing, which was not a young activity even back then.