Well, it could have been a lot worse. About 5.6 percent worse, if you do the math.

As we here at The Next Platform have been anticipating for quite some time, with so many stars aligning here in 2017 and a slew of server processor and GPU coprocessor announcements and deliveries expected starting in the summer and rolling into the fall, there is indeed a slowdown in the server market and one that savvy customers might be able to take advantage of. But we thought those on the bleeding edge of performance were going to wait to see what Intel, AMD, IBM, Qualcomm, and Cavium are going to bring to bear with their respective X86, Power, and ARM processors. And we think that one of the big hyperscalers that is also a cloud player has got the jump on the entire market when it comes to Intel’s impending “Skylake” Xeon processors, which are due within the next month or so according to the scuttlebutt.

Each new generation of processors is supposed to present a big jump in performance as well as an improvement in price, so it is not just a matter of getting a public relations coup to be put at the front of the line for any new chip generation from Intel and, now, its reinvigorated competitors in the X86, Power, and ARM arenas. Over the past several generations of Xeon chips, as we have shown in our past analysis, Intel has increased the performance the Xeon line by using a mix of architectural changes in the cores and caches to improve instructions per clock as well as by cramming more and more cores on the die to boost the throughput. But in many cases, thanks to the lack of credible competition, Intel has been able to hold the cost of a unit of performance more or less steady and therefore extract a lot of profits from the server base. In fact, we think Intel not only grew its profits from servers, but is and has been for a long time the main beneficiary, in terms of profits, from the system market. Microsoft and Red Hat get their piece of the action with operating systems, but the server makers themselves – whether they are OEMs or ODMs – live on skinny to no margins. A condition, by the way, that we think is unhealthy.

In presenting its server revenue and shipment report card for the first quarter, the analysts at IDC said that one large server customer making a big bet on cloud services accounted for approximately 250,000 units deployed during that period, which works out to 11 percent of the 2.21 million server units deployed. If you take the average selling price of a server sold by one of the ODMs – just shy of $2,800 and just a smidgen lower than a year ago – then this would work out to around $690 million in revenue, and if that hyperscaler – who we think is Google based on a hunch – did not have access to what we presume are Skylake processors, then revenues for the quarter would have been down by more than 10 percent and shipments would have fallen by 11 percent. This would have been a Mini Ice Age in the server market, albeit much less severe than the 30 percent to 35 percent declines we saw over four quarters during the Great Recession back in late 2008 and early 2009.

We think that Google is the big server buyer that IDC is referencing because it has been very vocal about having early access to the Skylake chips, and by virtue of the server volumes that Google is deploying as it builds out its Cloud Platform public cloud, it can move to the front of the Skylake line. To our way of thinking, Google dabbles in Power and ARM architectures but doesn’t make a big deal about it, as Microsoft has done in recent months. It is probably not a coincidence that Microsoft endorsed Qualcomm Centriq ARM chips as well as AMD Epyc X86 chips in its “Project Olympus” Open Compute servers at the same time as it announced support of Windows Server on ARM and Hewlett Packard Enterprise, which has Microsoft as one of its largest customers, stomached a 14 percent server decline in its first quarter. The ODMs were up strongly, too, and that also points to Google, which uses ODMs to build its iron. Whoever the hyperscaler is that got a half million chips from Intel – and it makes no sense that they are not Skylakes – they seemed to have soaked up all of Intel’s capacity to make the chips, which is why they are being announced sometime this summer instead of last fall or this spring.

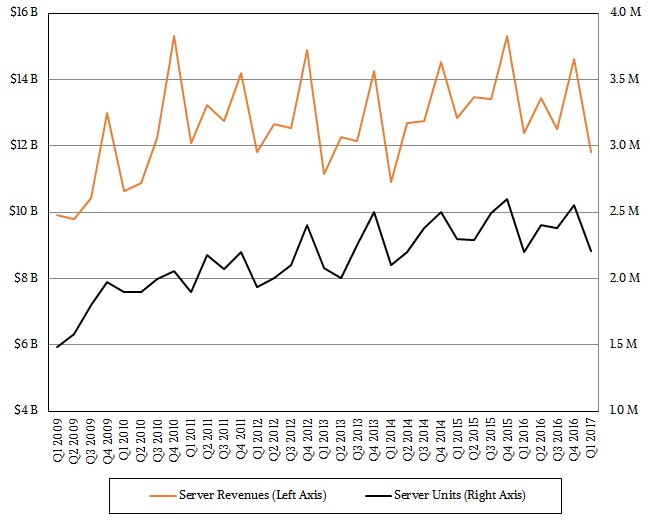

As it turns out, server shipments worldwide rose by 1.4 percent to 2.21 million units, according to IDC, but because of secular declines in the proprietary mainframe and midrange markets as well as in RISC/Unix platforms, revenues fell by 4.6 percent to $11.81 billion in the thirteen weeks ending in March of this year.

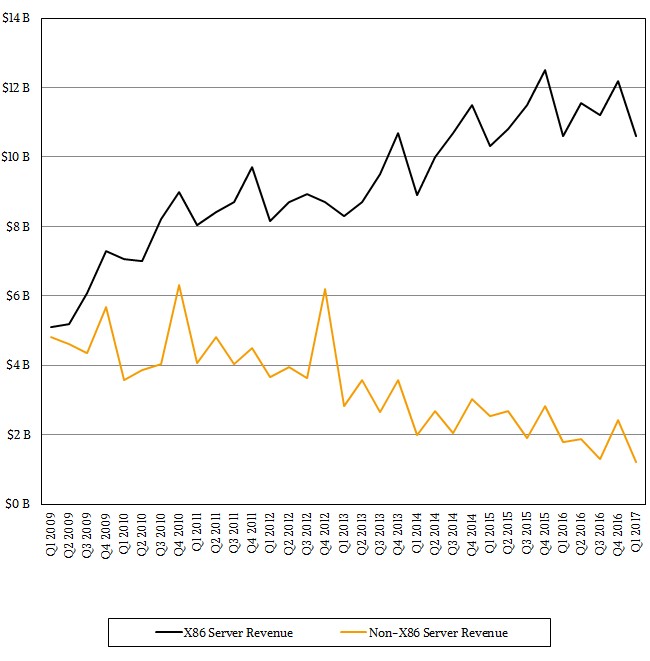

If you drill down into the figures, revenues for X86 machinery were flat at $10.6 billion and shipments held steady, too, which is remarkable if you think about it. The average selling price of an X86 server held steady at around $4,800 and change, and the funny bit to us is that the average X86 server costs about $2,000 more than the average ODM server. If you work the math out backwards, the tens of millions of enterprises that buy machines for their own use are paying a hefty premium for their gear, and not for nothing. They have a lot of redundancy and resiliency in each machine, since each machine tends to be mission critical and host its own applications and databases. (We are oversimplifying a bit.) This is why hyperscalers and cloud builders put resiliency in their clusters, but if you are replicating data and compute two or three times, notice how the price doesn’t really go down? If you give people utility pricing, they turn it off and on and reserve it, but then they end up using more of it, too.

Welcome to the IT industry. The price never really goes down. The functionality really does go up, however.

If you look at the server market by form factor and price band, the volume segment, which includes machines that cost less than $25,000, had a 3.4 percent decline in the first quarter, to $9.5 billion, and the midrange sector, which is comprised of machines that cost between $25,000 and $250,000, had a stunning 16.5 percent increase to $1.3 billion. (The midrange as so defined has not seen good growth in a while.) The high end of the market, with machines that cost more than $250,000, had a 20 percent decline to $1 billion. We can remember when this was how much money sold each month in System z mainframes alone.

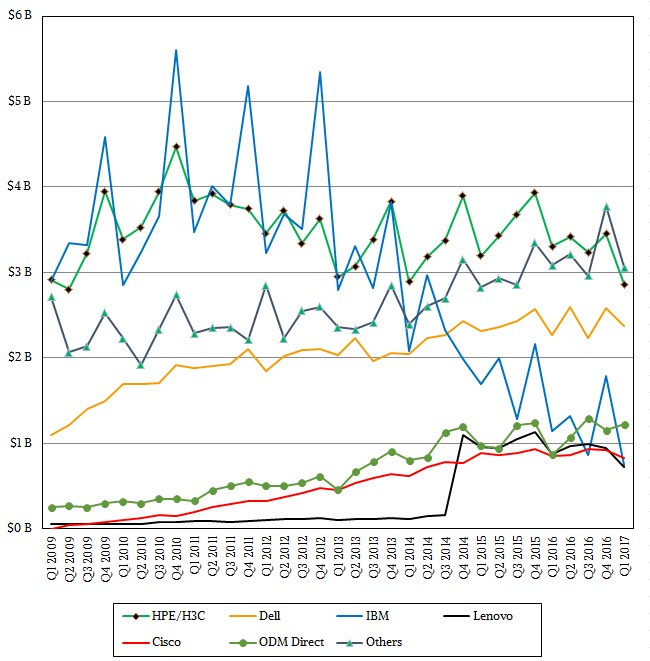

Hewlett Packard Enterprise has held onto its top spot in the revenue rankings, but even with the combination of its H3C partnership in China with Tsinghua University, HPE had a 15.8 percent revenue decline in the quarter, to $2.86 billion. Dell managed to eke out 4.7 percent growth to hit $2.37 billion, and that was because it grew shipments by a tenth of a point to 465,300 units. HPE’s units fell by 14.3 percent to 460,400 units, and the difference seems to be one of its big tier one customers, who we think was probably Microsoft Azure. Dell has been ahead of HPE in the market in the United States in terms of shipments for a while, and now it has beat it on the global scale.

Lenovo, on the other hand, is losing ground. The company’s shipments fell by 27.3 percent to 146,100 units and its revenues fell by 16.5 percent to $727 million, as best as IDC can reckon. IDC believes that Cisco sold $824.7 million in its UCS blade and rack systems in the quarter, down only 3 percent and doing better than the market at large, but clearly Cisco has found its water level at somewhere around $3.5 billion in annual server sales. IBM, which sold off its X86 server business to Lenovo, dropped the most in the first quarter, with revenues off a recession-like 34.7 percent to $744.5 million.

The ODMs, which IDC tracks as a group and which includes the likes of Quanta, Wistron, Foxconn, Tyan Jabil Circuit, and a few others, did remarkably well, with revenues up 41.8 percent to $1.22 billion and shipments up 44.1 percent to 443,600 machines. Again, we think that big hyperscaler buying what we presume are a quarter million Skylake machines is one of the big factors here.

The question we have now is whether the global market can consume a massive surge in computing power that is coming down the pike. If these impending CPUs are priced aggressively against each other, this will be great for price/performance, but not so great for chip makers unless there is elastic demand for compute. Form factors, persistent memory, and augmented compute through GPUs and FPGAs are compelling changes in the way systems are architected, too. It will be fascinating to see how this all plays out.