When we said thirteen weeks ago that we thought that Nvidia’s datacenter business would be its largest operating division before too long, we didn’t think it would only take a quarter to do that. But, as the gamers are awaiting the next-generation GPUs to power their ever-more-lifelike experiences and as systems using the “Ampere” A100 GPU accelerators, launched in May, ramped very aggressively and Mellanox switching contributed to the top line, too, in the second fiscal quarter ended in July, Nvidia’s datacenter business bypassed its gaming business in one giant leap.

Like this:

Thus pointing out the sometimes dubious nature of extrapolating future conditions from then-present ones. But we would also point out that this ascension is not going to last into the third quarter, and Nvidia said as much. This is a local maxima in a short time horizon, not a permanent one. At least not yet.

This is particularly true in the datacenter businesses that Nvidia participates in, where sales to hyperscalers, cloud builders, HPC centers, and large enterprises can be choppy depending on the place we are at in any GPU accelerator’s product cycle. Sometimes all of these sub-markets rise at the same time, at other times they all wiggle up and down at their own rates, and it is very hard to predict because, ultimately, what we are predicting is the summary of human behavior in distinct parts of the economy.

The rides up on the revenue roller coaster are fun, as any HPC system vendor can tell you, but steep declines can be gut-wrenching when they come. And they always come. You just have to be in your safety harness and brace yourself for them. But for now, Nvidia’s datacenter business is up like a rocket.

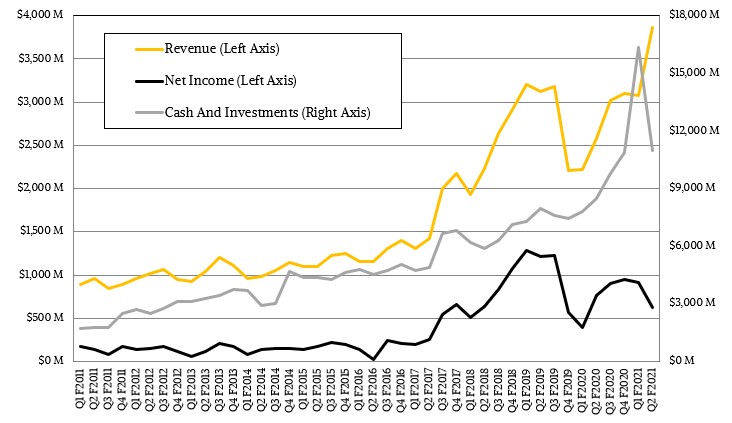

In the second quarter, Nvidia’s overall sales rose by 49.9 percent to $3.87 billion, helped considerably by the addition of the Mellanox networking business but also thanks to plenty of organic growth as well with the launch of the A100, which actually started shipping in the prior quarter but was ramping fast in the one just ended. Nvidia’s net income fell by 18.4 percent, however, to $622 million, or about 16 percent of revenues, the lowest profit share Nvidia has seen since the cryptocurrency market ran out of gas in the first quarter of 2020 and sales to hyperscalers and cloud builders also slowed a bit and sales overall dropped by 30.8 percent and net income dropped by 69.3 percent.

Drilling down into the numbers, the new Graphics group at Nvidia had $2.09 billion in sales, up 15.6 percent, and operating income rose by 28.9 percent to $911 million. The new Compute and Networking group, which Nvidia created in the wake of the Mellanox acquisition, had sales of $1.78 billion, up by a factor of 2.3X and had an operating income of $691 million, up 3.2X. The company booked a $951 million operating loss on its books, which includes stock-based compensation expense, corporate infrastructure and support costs, acquisition-related costs, legal settlement costs, and other non-recurring charges and benefits” according to the 10Q filing that Nvidia filed with the US Securities and Exchange Commission. In other words, rather than apportion these costs proportionally across these two groups, they are pulled out as a separate item across the whole company, with the idea of showing the underlying profitability of the two groups in isolation of all of that. We will let the accountants argue about whether or not this is sensible. You could argue either way, and at the very least it would be interesting to see what these charges are.

The main point is this: That Compute and Networking group is growing and is almost as profitable as the Graphics Group, with 38.8 percent of revenues falling to the middle line in the former compared to 43.7 percent of revenues for the latter.

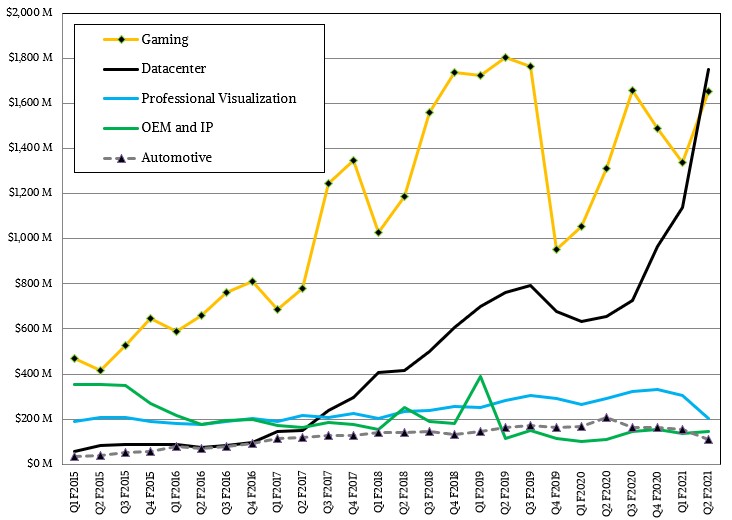

Using the old-style categories of revenue that Nvida has used since 2015 and that we hope it will continue to use, you can see how the segments stacked up in the chart above at the beginning of this story. The Datacenter unit was up 2.7X to $1.75 billion, and we are curious if the difference between the two is Quadro and GeForce cards that Nvidia knows are being used for compute since this is a slightly smaller number. (The difference was $29 million this quarter and $33 million in the first quarter.) Gaming GPU sales rose by 26 percent to $1.65 billion, while Professional Graphics fell by 30.2 percent to $203 million. Automotive was off 46.9 percent to $111 million, and OEM and IP rose by 31.5 percent to $146 million. What is clear from these two sets of numbers is that most of the OEM and IP revenue is being allocated into the Graphics group. A chunk of Automotive related to infotainment systems goes into Graphics and the chunk related to self-driving cars goes into Compute; we don’t know the split. This means there must be pretty sizable sales of something graphics in nature that went into the datacenter and not compute or networking or the numbers across the two categorizations could not pan out. GRID software for desktop virtualization is one such thing, for instance. These lines are sometimes hard to draw. Is a game console compute or graphics, for instance?

Gaming is up because people are spending to amuse themselves, which is obvious during The Great Infection. Ditto for Professional Graphics, as people are not going into the office where they might have worked on a rocketsled. Now, they are upgrading their home machines for fun and work. Automotive is down because worldwide car production is down, but not as bad as Nvidia had been expecting.

In Datacenter, Nvidia said that Mellanox accounted for 14 percent of sales and just over 30 percent of Datacenter revenue. To make the numbers converge, you get around $531 million with 13.7 percent of overall revenues and 30.3 percent of Datacenter, but this is obviously not the only convergence point possible. There was not a lot of detail given about the Networking division, except to say that Ethernet product shipments set a new record, driven by a build out among hyperscalers and cloud builders, and InfiniBand sales were also up year on year.

If you do the math, then the Datacenter business minus Mellanox accounted for $1.22 billion in sales in the second quarter of fiscal 2021, and nearly doubled from the $655 million posted in the year-ago period. This is sales of all of the GPU accelerators (formerly lumped under the Tesla brand) and the HGX component and DGX system sales that Nvidia has as well. The Ampere A100 ramp is very steep, according to Nvidia, with more than 50 servers configured with it at the moment and another 30 during this summer and more than 40 more slated for adoption by the end of 2020, according to Collette Kress, Nvidia’s chief financial officer, who divulged this during the call with Wall Street analysts. She added that A100-related products drove under 25 percent of Datacenter revenues, which works out to somewhere under $438 million – but significantly, not a small number at all and we think probably 2X that A100-related produce sales that happened in the first fiscal quarter, ahead of the formal launch in May. (Nvidia was shipping A100 stuff in January or February, we think, perhaps earlier.) If you peel out Mellanox and A100 stuff, the rest of the Datacenter is stuff, based on early GPU technology, still accounted for around $785 million in the quarter.

This Nvidia datacenter business doesn’t turn on a dime to new technology, just like that of every other datacenter supplier in the world. Transitions are not discontinuities, but relatively smooth curves.

Kress threw out a few milestones in her presentation. First, Nvidia has shipped over 1 billion GPUs capable of running the CUDA GPU acceleration offload framework, and the total number of developers who are programming in CUDA or other environments aimed at GPU acceleration is now over 2 million. It took a decade to reach the first million and only two years to add on the second million – and that is very steep exponential growth.

Looking ahead, Nvidia expects that revenue in the fiscal third quarter ending in October will be $4.4 billion, plus or minus 2 percent, which works out to somewhere between $4.31 billion to $4.49 billion if you do the math and think you can increase the significant digits to four on a number that has only two to start with. (This is not exactly valid math, and it would be nice if Nvidia gave three digit estimates of revenues and just said them.) The Datacenter business is only expected to be up in the “low-to-mid single digits” according to Kress, but gaming, with a new GPU product cycle coming, it expected to rise 25 percent sequentially. Call it 4 percent growth for Datacenter sequentially, and you are at $1.82 billion in sales, and Gaming looks like it will cross the $2 billion mark. So Gaming will be back on top again. But the race is neck and neck, and before long, as we said, Datacenter will get bigger than Gaming and it has a very good chance to stay that way if Nvidia plays its cards right.

Until then, we suspect there will be lots of local maxima for both Gaming and Datacenter, and hence our use of the plural.