Just as in so many other areas of the world economy where real growth is being driven by those who can afford the bleeding edge, chipmakers are seeing the greatest opportunity at the top end of the market.

While the lower end of the semiconductor industry has its own challenges, the server farm builders are supporting fresh growth for Taiwan Semiconductor Manufacturing Company (TSMC).

The “HPC” designation in the headline likely caught the eye of those in the supercomputing world but for TSMC , high performance computing (HPC) includes all high-end server processors, from CPUs to GPUs, no matter what the end use cases.

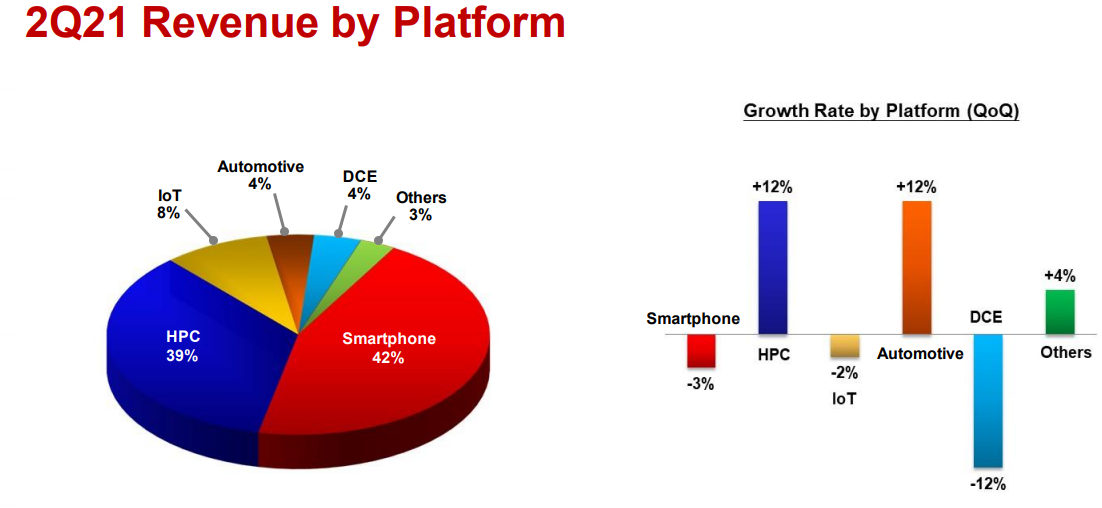

The semiconductor manufacturer says their second quarter revenue, which increased 2.9% was supported by the high-end server chips business and to a slightly lesser extent, automotive-related demand. HPC increased 12% to account for 39% of TSMC revenue while other historically important areas like IoT and smartphone were down (2% and 8% respectively).

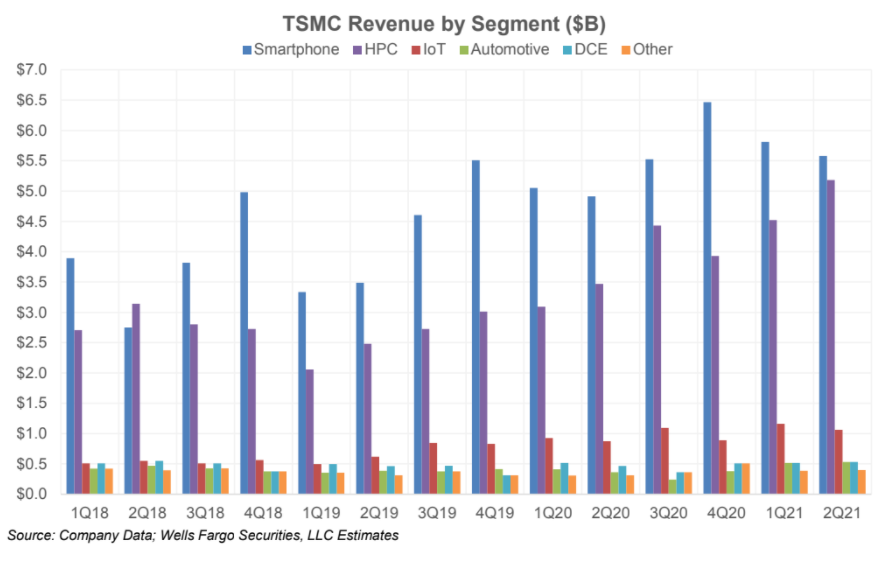

Wells Fargo analysts put together a chart showing the growth of the HPC segment for TSMC since 2018, which highlights the value of the 5nm addition to TSMC’s lineup.

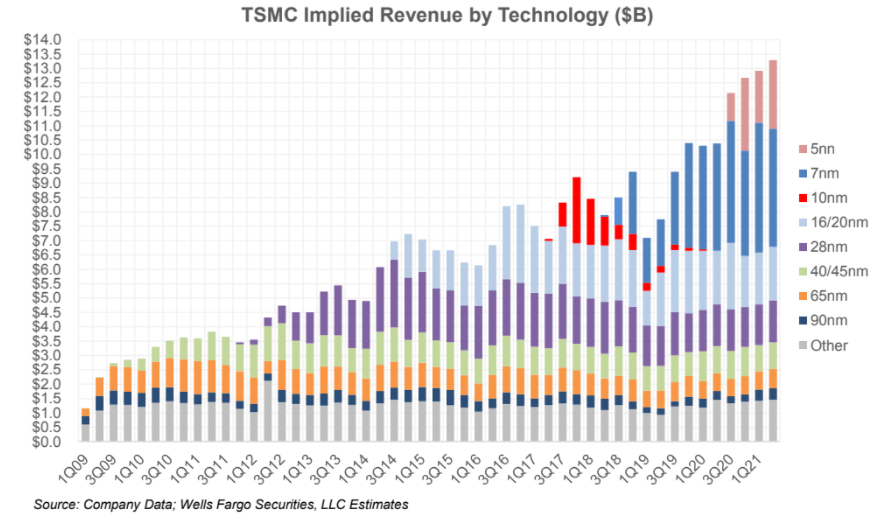

The company’s 5nm and 3nm roadmaps are critical to even greater improvements. TSMC’s 5nm FinFET process, which came online in volume in mid-2020 is core to both HPC and smartphone business. The company also announced that its N4 (4nm) technology will provide further gains in density for 5nm but that will not be available until 2022.

In its earnings call, TSMC’s VP and CFO, Wendell Huang, said N5 is in volume production with yields well on track. “N5 demand continued to be strong, driven by smartphone and HPC applications and we expect N5 to contribute around 20% of our wafer revenue in 2021.”

Huang also points to the N3 roadmap, noting, “technology development is on track with good progress. We have developed a complete platform support for both HPC and smartphone applications of N3.” He adds that TSMC continues to see “a high level of customer engagements at N3 and expect more new tape-outs for N3 for the first year as compared with N5.”

Moving into third quarter 2021. We expect our business to be supported by strong demand for our industry-leading 5-nanometer and 7-nanometer technologies driven by all 4 growth platforms, which are smartphone, HPC, IoT and automotive-related applications.

Aaron Rakers and his team of equity analysts at Wells Fargo noted that the company expects its customers to exist the second half of 2021 with a “healthy level of inventory relative to historical seasonable patterns” but adds that the company “did not rule out a potential inventory correction as customers build inventory” over that span. TSMC expects to remain capacity constrained throughout the rest of the year and into 2022.

As a reminder, TSMC previously noted it expects its 3nm to see around 70% logic density gains and up to 15% performance improvement; up to 30% power improvement versus 5nm.

Rakers and team highlight TSMC comment that they will be raising wafer prices due to manufacturing cost increases, especially for leading-edge nodes in addition to investing in older nodes, especially given hikes in materials and commodity costs.

In the bigger picture, TSMC expects revenue in Q3 to be between $14.6 and $14.9 billion.

Rakers and team add that due to strong customer demand TSMC plans to expand in its northern, central, and southern science parks in Taiwan. “TSMC’s Arizona fab was noted as on track with equip move-in scheduled for 2H2022 (20k wspm; 5nm), noting it has not ruled out a potential 2nd phase over time. TSMC confirmed its 28nm capacity expansion in Nanjing, China (targeting 40k wspm by mid-2023), while the company is in the diligence process for a potential Japan fab.”