One of the more interesting trends in infrastructure that we try to get a handle on every once in a while is how much of the server and storage capacity is being deployed in bare metal, standalone fashion and how much is being sold to run utility style, cloud environments. It is very difficult to suss this out, and the market researchers and forecasters at IDC take a stab at this every quarter, usually a quarter behind the statistics they put out for raw server, storage, and networking gear shipments and revenues.

It is a lot harder to make such fine-grained distinctions and it takes more time, we presume. We like to riff on this research, as we did back in July when the cloud and non-cloud infrastructure sales figures were released for the first quarter of 2021. We are not going to repeat everything we said at that time about what this all means – read the story, called Cloud Is The Dominant Platform Consumption Model – So What?, for our thinking – but we did want to update you on the Q2 2021 numbers, where there was a slump in infrastructure sales for both cloud and non-cloud gear and also talk a bit about how hyperscalers, cloud builders, and other kinds of service providers have come to dominate the buying of infrastructure.

Just as a reminder: Last quarter, IDC launched a new Worldwide Quarterly Enterprise Infrastructure tracker that brings together revenues for servers and storage for systems, eliminating some of the double-counting that was done in its independent server and storage trackers. This new tracker also breaks the market down into infrastructure that is cloud and shared, cloud and dedicated, and non-cloud and dedicated. In the past, we might have called these public cloud, hosted, and on-premises and traditional IT systems. But there are nuances of difference. Non-cloud and dedicated systems can be on premises or in a co-location facility, for instance. Cloud and dedicated can be an AWS Outpost, a Microsoft Azure Stack, or a Google Anthos cluster running at your site. This new way of thinking by IDC is removing the where of the compute and storage and focusing on the how of compute and storage.

Also, the new tracker from IDC is concerned with the spending by the organizations that build this infrastructure, and doesn’t differentiate from corporate, government, or public cloud spending. This is not a measure of the value of what the public clouds sell, but the investment that public clouds make. And this data is presented by vendor, which is useful, and also has updated its forecast, which now runs from 2020 through 2025, inclusive.

Let’s start at the top and drill our way down. In the second quarter of last year, the coronavirus pandemic spread around the world and companies invested a huge amount of money in adding infrastructure to provide services to all of us living a more digital life than we ever had before and also to work from home. So it is not a surprise at all that spending would eventually cool on infrastructure, considering it was up by 55.5 percent in Q2 2020 by the hyperscalers and cloud builders. In Q2 2021, spending on both dedicated and shared cloud infrastructure fell by 2.4 percent to $16.8 billion. Within this, spending on infrastructure that went into shared clouds – meaning what we often call a public cloud – fell by 6.1 percent to $11.9 billion. Spending on dedicated cloud infrastructure – meaning what we called on-premises cloudy gear as well as outposts that clone the gear of public clouds but located on premises or in a co-location facility – actually rose by 7.8 percent to $4.9 billion. And of this, 46.5 percent of the total – or $2.28 billion – was deployed at customer sites rather than in co-location facilities.

Sales of non-cloud, traditional host systems comprised of bare metal servers and storage also rose in the period, in this case by 3.4 percent to $13.4 billion, just the opposite trend we have seen in cloudy infrastructure. Both now, and a year ago, too, when non-cloud infrastructure sales fell by 7.2 percent.

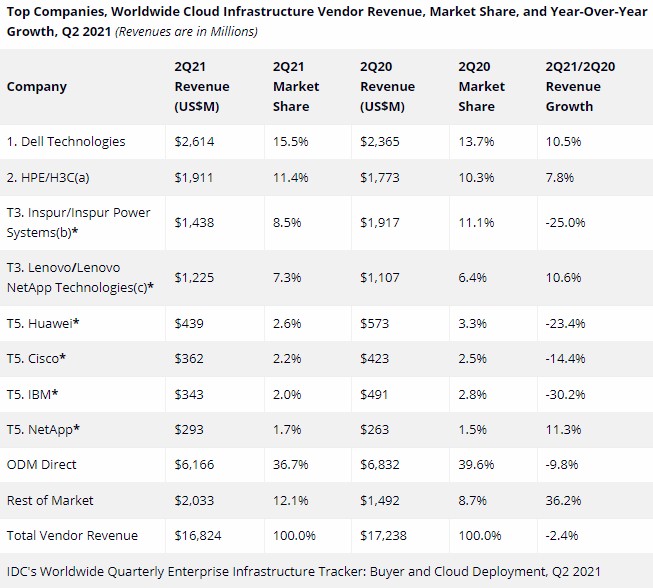

When you factor out the overlapping server and storage sales – plenty of storage arrays are made of servers and so you have to be careful of the double counting that is inherent in the raw server and storage data the comes out of both IDC and Gartner – Dell is the dominant supplier of cloudy infrastructure, followed by Hewlett Packard Enterprise, Inspur, Lenovo, Huawei Technology, Cisco Systems, IBM, and NetApp. As a group, the original design manufacturers (ODMs) that supply the gear to the hyperscalers and biggest cloud builders, are the biggest suppliers in the market, and while it is interesting to use this as a kind of proxy for spending by hyperscalers and cloud builders, it is not a very good proxy since plenty of the Super 7 – Google, Amazon Web Services, Microsoft, Facebook, Alibaba, Baidu and Tencent – buy gear from OEMs as well as ODMs, and Dell, Lenovo, and Inspur have ODM-like businesses that are not counted in that total for ODM server and storage makers. In any event, here is the play by play for cloud infrastructure sales – adding sales of infrastructure for both dedicated cloud and shared cloud together – for the second quarter:

Dell, HPE, and Lenovo grew, probably on the strength in spending among enterprise customers buying cloudy servers and storage, but some vendors, as the chart above shows, took it on the chin in Q2.

Here’s an interesting set of tidbits. IDC also tracks the spending of cloud and non-cloud gear by service providers, and it is using that term in the broadest sense meaning what we call hyperscalers and cloud builders as well as telco and other kinds of service providers. In the second quarter of 2021, this broad service provider category spent $17.06 billion on gear, down 1.9 percent from the $17.39 billion the service providers collectively spent in the year-ago period. While the trend is down a bit because of muted spending by the hyperscalers and biggest cloud builders, together the service providers are wagging the server and storage markets by their tails.

While Q2 was a bit of a bummer for infrastructure sales, IDC says that it still expected for cloud infrastructure spending to grow by 12 percent to $74.3 billion for all of 2021. Within this, shared cloud infrastructure sales are anticipated to rise by 11.1 percent to $51.4 billion and dedicated cloud infrastructure sales are expected to rise by 14.1 percent to $22.8 billion for all of 2021. While much has been made of the long-term trend towards cloud infrastructure and away from standalone, hosted, non-cloud servers and storage, this traditional part of the IT market is expected to grow by 2.7 percent to $58.9 billion.

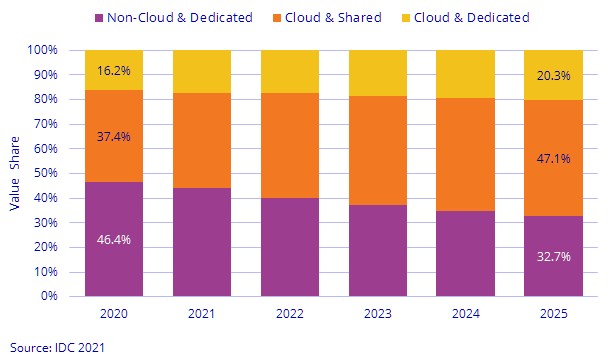

And as the chart above shows in the forecast out to 2025, it is going to take a long, long time to get rid of traditional, standalone, bare metal hosts that are more like pets in the datacenter, with all of their uniqueness and mission criticality than they are like the massive herds of cattle that are in hyperscaler and cloud builder datacenters. At some point in the future, maybe in 2030 or 2035, maybe this way of computing will go away. Or, maybe it will just live on forever as a niche for doing back office stuff. We were born in the mainframe era, and there is a good chance that when we colonize Mars, the payroll will be done by some punch card walloping mainframe that is gussied up to look like an iPhone XXVI with a pretty neural interface or some such nonsense.

It took a long time for the continents to converge to create Pangea, squeezing out the ocean. And the thing to remember is that supercontinents always drift apart to create new oceans.