Hewlett Packard Enterprise has always been more interested in providing a choice of compute engines compared to Dell, which was the underdog in servers for a long time. Now, HPE is the underdog in general purpose serving but thanks to the acquisitions of SGI and Cray is the dominant supplier of traditional HPC simulation machines, and it has to be friends with any vendor that sells an AI engine, but these companies are hostile to each other.

It is much easier to be Dell, but for customers, perhaps it is better to have an HPE not only to compete hard against Dell, but to help navigate the complex decision matrix of XPU supply chains across vendors.

HPE has its work cut out for it to catch Dell in the early days of enterprise adoption of AI servers, even with its very deep and broad supercomputing experience.

Dell sold $1.7 billion of AI systems in its most recent quarter ended on May 3, as we reported last week, a 10X increase in sales compared to the year ago period. That was a factor of 2.1X sequential growth for AI server revenues, which is pretty good but which is also more indicative of GPU allocations from Nvidia than anything else.

Importantly, Dell’s margins were actually hurt by those AI server sales, although the company did not say by how much. Non-AI servers at Dell were up 7.2 percent to $3.77 billion, but we don’t know margins specifically on this iron or the AI servers. What we do know is that Dell’s Infrastructure Solutions Group had a 21.5 percent increase in sales of servers, storage, and networking in the May quarter, but operating income was actually down a half point to $736 million. For all we know, profits on all of its ISG lines were down, or some were up and others down more sharply.

The story is much the same at HPE. In the quarter ended April 30, HPE’s AI servers more than doubled more than $900 million, according to Marie Myers, HPE’s chief financial officer, who went over the numbers for the April quarter (which is roughly the same one that Dell completed) with Wall Street along with chief executive officer Antonio Neri. Our model shows HPE AI server sales rising by 2.6X to $907 million and increasing by 2.2X sequentially. HPE has been selling pre-exascale and exascale GPU-accelerated supercomputers for many years and Dell has not, which is why its growth seems more astonishing. But what is more significant, we think, is that Dell was able to get enough allocations of GPUs to deliver – and therefore book revenue for – nearly twice as many AI servers as HPE.

And, like Dell, it doesn’t look like the additional AI server revenues are significantly boosting the profits of its core systems business.

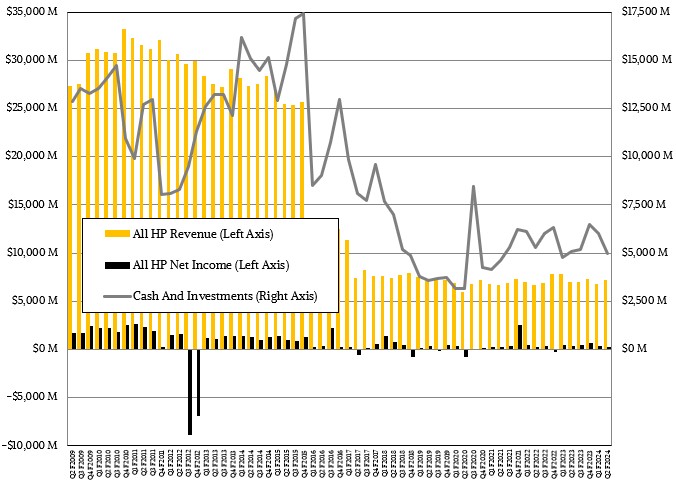

HPE rejiggered its financial reporting groups and divisions once again last quarter, so we don’t have the same insight into generic server sales and HPC/AI system sales like we used to. What we can tell you is that overall sales in the Server group were up 17.6 percent, but earnings before taxes for the Server group were down 9.9 percent. Once again, we cannot tell if AI servers are less profitable than even HPC systems, which historically have moderate profits or losses in any given quarter and a tiny smidgen above break even over the long haul. It could be that general purpose servers, HPC systems, and AI systems are all under pricing pressures and are loaded up with costs that are making profits hard to come by.

We have said many times before that no one has ever gotten rich in the HPC business, and we stand by that observation. But we are going to amend it. No one except Tom Tabor.

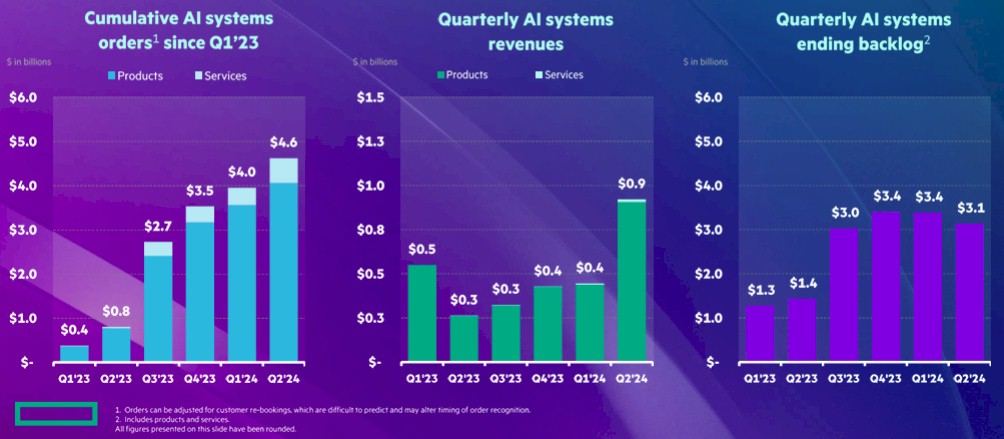

To provide a little more insight into its AI server business, HPE created this gem of a chart, which shows cumulative AI system orders since the first quarter of fiscal 2023 ended in January of that calendar year as well as AI system revenues booked in each quarter and the AI system order backlog for each quarter. Take a look:

We wish HPE would just put out these real numbers with at least four significant digits and be done with it, but we did out best to reconcile our prior estimates with these heavily rounded numbers to come up with a model.

The way we see it, there are two things that are holding HPE back when it comes to AI servers. First, all of the “Antares” Instinct MI300A hybrid CPU-GPU accelerators that AMD could have made went into the “El Capitan” supercomputer being built by HPE for Lawrence Livermore National Laboratory. And nearly all of the Antares Instinct MI300X that AMD can ship went to the hyperscalers, notably Microsoft and Meta Platforms. Nvidia is happy to work with HPE on supercomputers based on its “Grace” Arm server CPUs or Grace-Hopper hybrid CPU-GPU superchips, but we think Dell is getting preferential treatment for being a loyal Nvidia proponent for HPC and AI systems. Perhaps the difference in AI server revenues comes down to which company has customers with money, electricity, and cooling for the GPU machinery. It could be that simple.

What we do know is that Dell and HPE need to sell AI servers and figure out how to do it profitably, and Nvidia needs Dell, HPE, and other original equipment manufacturers to spread the GenAI religion and hardware to the masses. This where the OEMs hope some real profits can be made, if history is any guide. But Nvidia could keep all of the profits for itself and make the OEMs get their profits in services and tech support, much as Intel did with server CPUs for the better part of a decade. This certainly looks like what is happening with GPU systems for HPC and AI workloads right now, and we are think when HPE and Dell can’t make profits on selling training systems, they will try to make profits on inference systems.

We shall see how that works out. We are hopeful for their sake, but doubtful given the history of low profits for the OEMs.

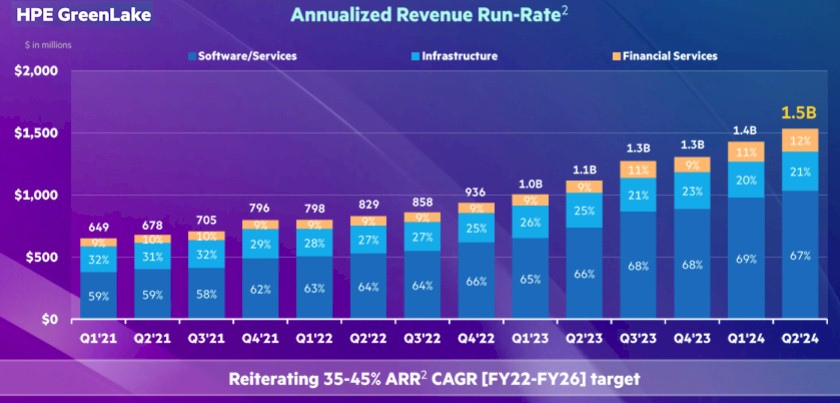

In the meantime, HPE is going to stick to its GreenLake cloud-like pricing for infrastructure and try to be the kind of systems vendor millions of companies around the world still need because they cannot buy in high volume and yet they want to control their own infrastructure and their own fates.

The GreenLake customer count increased by 9 percent sequentially to 34,000 organizations around the world, and the lifetime contract value of GreenLake deals is more than $15 billion. The annualized run rate – a hypothetical number that says take the current quarter and multiply by four to get a quasi-realistic size of the business – is up 39 percent to $1.5 billion. And significantly, two third of that is driving sales of software and services, not iron. That is another way of saying people want to pay subscriptions for software and services, but they are still getting used to doing so for hardware. It is also likely that a lot of GreenLake hardware deals have a lot of HPE software and support added in.

As always, through the many decades that Hewlett Packard has been a system vendor and acquired others – Compaq, DEC, Tandem, SGI, and Cray are the biggies – what is important is that HPE make some money out of its core systems business. It is still doing that:

In the April quarter, we estimate HPE’s core systems business – servers, switching, storage, systems software, tech support, and financing – was up 9.2 percent to $5.77 billion, which was up 9.8 sequentially largely due to AI servers. But operating income fell by 9.6 percent to $509 million in our model and was only about 8.8 percent of revenues. From Q1 of fiscal 2018 through now, HPE has sold $152.9 billion in systems stuff into the datacenter and it has brought $16.6 billion of that to operating income, which is about 10.9 percent of revenues. So HPE is actually running a bit lean right now, which happens from time to time.

Over that same timeframe, Dell has sold $227.7 billion in IT gear and brought in $26.5 billion in operating income, which works out to being 11.6 percent of revenues. But in Dell’s most recent quarter, its datacenter operating incomes were only 8 percent – even leaner than HPE’s were.

This is a tough business, but at least it is not as bad as retail. . . .

HPE is optimistic about its future prospects, as it always is.

“We expect a materially stronger second half led by AI systems, traditional servers, and storage, networking and HPE GreenLake,” explained Neri on the call with Wall Street. “Let me recap the key drivers that factor into our expectations for Q3 and the full year. For server, we expect improving GPU supply for AI systems and improving demand for traditional servers to drive sequential revenue increases through fiscal year 2024. While the rising AI systems mix is a gross margin headwind, we are balancing this with higher margin services revenue, improving scale, and cost discipline. We expect the segment operating margin to be approximately 11 percent for the fiscal year.”

Looking ahead, HPE expects for sales in its third quarter ending in July to be between $7.4 billion and $7.8 billion, which is 10 percent growth at the midpoint. The shift from Aruba networking to AI systems is hurting margins – that wireless networking business accounted for half of HPE’s operating profits for a while there – and the slowdown in the Intelligent Edge group has been especially hard in recent quarters.

As we have said before, it would help all of the OEMs if Nvidia would share some of the wealth. If Nvidia does not do that, they will seek – and find – alternatives.