Welcome to the most important earnings call in history, with the weight of the aggregate stock markets of the entire world hanging on what Nvidia says and doesn’t say. Well, the most important one until thirteen weeks from now.

And get used to that cadence until this GenAI boom either goes bust or normalizes to a high percentage overall IT spending. Which means for the foreseeable future.

By the way, we think spending on generative AI will normalize over the long haul, and is something that we discussed separately with Nvidia’s chief financial officer, Colette Kress, after the numbers came out. We think that generative AI is cannibalizing some of the “regular” spending in IT for maintaining and updating traditional applications while at the same time expanding overall spending on IT much as the Internet boom did almost three decades ago.

But as we say, that is a separate story. This one is a drilldown on Nvidia’s financial results for the second quarter of fiscal 2025 and its forecasts for the rest of the year.

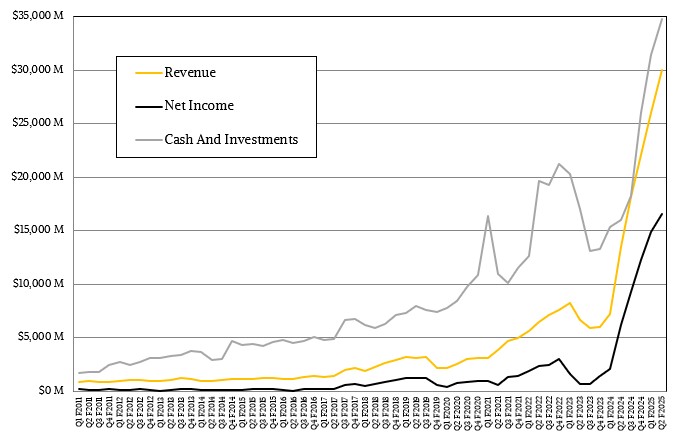

In the quarter ended in July, Nvidia’s overall sales were just a hair over $30 billion, up 2.22X compared to the year ago period. Which is still, when you think about it for more than a second, amazing.

But now Wall Street and the hoards of Nvidia investors who have made this one of the richest companies in history (if gauged by market capitalization) are used to that doubling, and they want more than a conservative guide and a consistent beat compared to Wall Street expectations. Why is a bit of a mystery to us. This gravy train is still trucking along, despite many obstacles.

Perhaps the hoards want a forecast that goes out five years and a stock price that reflects that guide so they can cash out and benefit from the rest of the AI revolution that has not even happened yet?

Such impatience. You have to let a story unfold, page by page, and live it. That’s what makes it exciting.

In the July quarter, operating income rose by 2.74X to $18.64 billion, and net income increased by 2.68X as well to $16.6 billion. That net income worked out to 55 percent of revenue, which again, is amazing and is consistent with the 51 percent, 56 percent, and 57 percent levels seen in the prior three quarters. Had it not been for a $908 million writedown, primarily for failed Blackwell GPU parts and detailed in Nvidia’s 10-Q filing with the US Securities and Exchange Commission, profitability would have been even higher.

We have said it before and we will say it again: Nvidia does not need to sell Blackwell now, and Hopper is more profitable in that it takes twice as many skinny memory Hoppers (96 GB) to do the work of a normal memory Blackwell (192 GB). As long as companies are desperate for GPUs – like Elon Musk’s xAI startup certainly was when it acquired 100,000 H100s for its new supercomputer in Memphis that is being built over the next several months – the H100 was perfectly acceptable. Because the alternative is. . . . well, there is not an alternative really at those volumes.

By the way, Kress confirmed what we suspected and that Nvidia got the deal for the back-end network for the “Gigafactory of Compute” system being built in Memphis, and it is indeed a Spectrum-X Ethernet setup with Spectrum X800 switches and Bluefield-3 DPUs.

Nvidia’s Datacenter division drove 87.5 percent of the company’s revenues. Frankly, the gaming GPU business is about a tenth the size, and the other three divisions – Professional Visualization, Automotive, and OEM and IP – are hardly visible anymore.

For a number of years now, Nvidia has been breaking its business into two groups, for which it provided some operating profits for a few quarters before it thought better of that (helpful) idea. We think Nvidia should also show the operating profits of the various divisions as well. Why not?

The Compute and Networking group had sales of $26.45 billion, up 2.54X compared to the year ago period. The Graphics group, which is made up of GPU cards sold to gamers and workstation users, had sales of $3.59 billion, up 15.7 percent.

Remember when graphics was Nvidia’s largest business? That was true just two years ago, and it will never be true again. Unless something really weird happens.

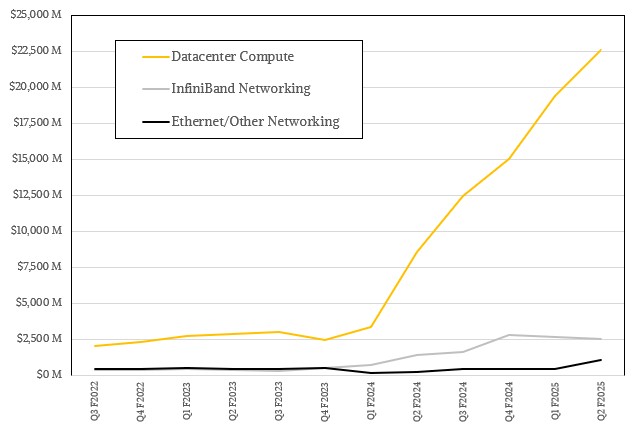

The datacenter business at Nvidia is what we really care about, so let’s drill down further. In the quarter, datacenter compute, a new category that Nvidia has been breaking out separately for the past several quarters and what we have been estimating since it acquired Mellanox Technologies in March 2019, accounted for $22.6 billion in sales, up 2.63X year on year. Networking was up 2.14X to $3.67 billion.

Our model shows that InfiniBand sales rose by only 75.4 percent to $2.58 billion and was actually down 5 percent sequentially, and that Ethernet and other networking (meaning NVSwitch interconnects) accounted for $1.09 billion in sales, up 4.51X. We think both Spectrum-X and NVSwitch are contributing to this part of the business, and we wish that Nvidia would explicitly break out InfiniBand, Ethernet, and NVSwitch sales. But it will not because hyperscalers and cloud builders are moving away from InfiniBand and towards Spectrum-X.

What we can tell you is that Kress said on the call with Wall Street analysts that Ethernet revenues specifically for AI platforms doubled sequentially from Q1 F2025, and hundreds of AI customers have adopted Spectrum-X.

When it comes to AI workloads, Nvidia said that more than 40 percent, or around $33.52 billion of sales, were for AI inference workloads in the trailing twelve months. We reckon that AI training has pushed $40.1 billion in sales, and HPC and other data analytics workloads accounted for around $8.18 billion.

For the trailing twelve months, datacenter revenues were up by a factor of 3.71X to $81.75 billion, and with sales of $32.5 billion plus or minus 2 percent expected in the third quarter and given somewhere around 88 percent of overall sales being driven by the datacenter, then it is reasonable to expect datacenter revenues of $28.6 billion in Q3 F2025. Assuming something akin to 15 percent sequential growth as Blackwell revenues kick in during Q4, then we expect somewhere around $110.33 billion in datacenter sales for Nvidia for fiscal 2025.

That means Nvidia will join Dell, Hewlett Packard Enterprise, and IBM as the only companies in the IT sector that have broken $100 billion a year in sales in the datacenter in all the history of IT. And we can tell you for sure that none of them were as profitable as Nvidia when that happened. (Although, if you inflation adjust IBM’s revenues from the late 1960s and early 1970s, you could see similar profitability for the venerable System/360 and System/370 mainframes. We will do that math someday to be sure. But not today.)

Which brings us to the much-rumored delays in the shipments for Blackwell GPUs. In her CFO commentary, Kress said the following:

“We shipped customer samples of our Blackwell architecture in the second quarter. We executed a change to the Blackwell GPU mask to improve production yield. Blackwell production ramp is scheduled to begin in the fourth quarter and continue into fiscal 2026. In the fourth quarter, we expect to ship several billion dollars in Blackwell revenue. Hopper demand is strong, and shipments are expected to increase in the second half of fiscal 2025.”

When asked if there were packaging or other issues with the Blackwell GPUs and the systems that use them – something that has been rumored and widely circulated – Nvidia co-founder and chief executive officer Jensen Huang had this to say:

“The change to the mask is complete. There were no functional changes necessary, and so we are sampling functional samples of Blackwell and Grace-Blackwell in a variety of system configurations. As we speak, there are something like a hundred different types of Blackwell-based systems that are built and that were shown at Computex, and we are enabling our ecosystem to start sampling those. The functionality of Blackwell is as it is, and we expect to start production in Q4.”

That seems to clear that up. To have such additional issues as were rumored and to not disclose them at this point would no doubt draw the ire of both investors and the SEC.