If you think it might be difficult to sell companies general purpose servers when they are frenzied about GenAI and trying to figure out how to get GPU-accelerated systems, you ought to try to convince the same companies to upgrade to Windows Server 2025, which launched last November.

Yes, that was two years after the GenAI big bang, but Microsoft’s on-premises server business, which is largely transactional in nature, is taking a backset to GenAI in general and to Azure in particular. And that means that the profits in its overall “real” systems business, which includes the Windows Server platform as well as the core infrastructure services of compute, storage, and networking that it sells on the Azure cloud, are under pressure.

That’s what we immediately see when we look at Microsoft’s second quarter of fiscal 2025, a thirteen week period that ended in December. And from the looks of things, it is not going to get any easier for Microsoft in the coming quarters, either.

Having said all of that, Microsoft has built one of the largest infrastructure platform revenue streams in the world – larger than Hewlett Packard Enterprise, Dell, or even Amazon Web Services and up there with IBM selling its legacy Power and System z mainframe platforms – and that is a thing to behold.

Why Apps And PCs Matter

Microsoft is a big, complex hairball of a thing, but it has three things – datacenter infrastructure, enterprise applications, and software for PCs – well under control. So long as we all don’t start thinking of Copilot as the next Clippy. (Which we do here at The Next Platform, for the most part.)

Let’s take Microsoft’s Q2 numbers from the top and drill down to the infrastructure core.

In the December quarter, Microsoft’s revenues rose by 12.3 percent to $69.63 billion, with operating income up 13 percent to $30.55 billion and net income up 10.2 percent to $24.11 billion. The net income level, which is what Wall Street really cares about, is not as sweet as usual, but is still in the low end of normal range for the Microsoft conglomerate. Due to its extensive investments in Azure cloud capacity – mostly, but certainly not exclusively, driven investments in AI clusters – Microsoft has been burning cash at a slightly faster clip than it is retaining it. In the quarter, the company shelled out $22.6 billion for the acquisition or leasing of datacenters and gear, with $15.8 billion of that going to property, plant, and equipment for Azure. The rest went for CPUs, GPUs, networks, and the stuff going into those datacenters.

Microsoft said on the call with Wall Street analysts that it would spend at around the same rate for the remaining two quarters in fiscal 2025.

The heavy capital spending is why Microsoft’s cash and investment hoard is down 11.7 percent year on year to $71.56 billion. A little more than a year ago, Microsoft had $143.95 billion in the bank. This is what heavy investment in AI has done to the Microsoft balance sheet. But, then again, that is what a balance sheet is for, and the company still has more money in the bank than most enterprises on Earth.

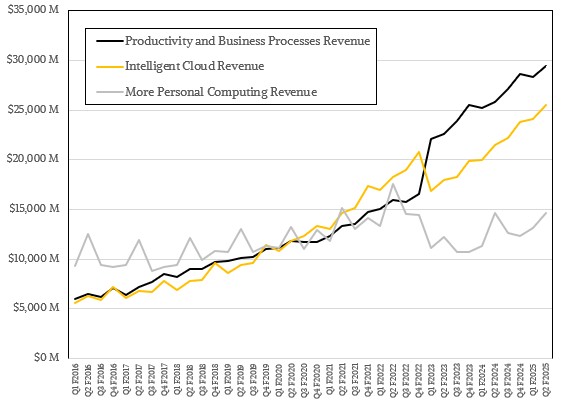

Microsoft thinks of itself these days as being comprised of three groups: One that sells application software, one that sells infrastructure hardware and software, and one that sells productivity tools and systems software for PCs. The Intelligent Cloud part – that’s the middle one that includes the Windows Server stack and Azure – is the one we care about directly, but we care about the other two indirectly inasmuch as if they are generating revenues and profits, the heat is off Intelligent Cloud to do more than its fair share of financial lifting.

Which is why everyone who uses the Azure cloud or runs Windows Server on premises should be thankful for the Productivity and Business Process application software group, which had $29.44 billion in revenues, up 13.9 percent, and operating income of $16.89 billion, up 16.3 percent. That operating income represented a very respectable 57.4 percent of revenue – close to what we call around here “Cisco-class operating incomes” when we run our own businesses. The More Personal Computing group – we are not sure what is more personal than personal – is that core PC business that is the heart of Microsoft, and it was flat at $14.65 billion in sales, but with $3.92 billion in operating income, up 32.2 percent, and representing 26.7 percent of revenues

Average these two out by adding them together, you get revenues outside of Intelligent Cloud that rose 8.9 percent with operating incomes up 19 percent. Again, a business that has income rising twice as fast as revenue and in the double digits at that is not too shabby.

Intelligent Cloud includes Windows Server, SQL Server, Visual Studio, and other middleware and tools sold into the datacenter as well as compute, storage, and networking capacity on the Azure cloud and related platform software and SaaS services Microsoft peddles into the datacenter and on Azure.

In the second quarter of fiscal 2025, Intelligent Cloud drove $25.54 billion in sales, up 18.7 percent, with operating income of $10.85 billion, up 13.6 percent. You see the squeeze there, and it ain’t coming from renting GPU capacity on Azure, we can assure you. That 42.5 percent of revenue for the operating income in Q2 F2025 is, however, running a little lower than average but not crazily so.

We think the general purpose server recession that has been happening since the GenAI boom hit in late 2022 – and that is only now starting to reverse because datacenters have figured out they have to consolidate old server gear onto much more efficient new server gear to find space, power, and cooling for AI systems – is still hitting Microsoft. If you consolidate servers, you need fewer server licenses. If you can do the work on fewer cores, you need fewer server licenses. And so, Amy Hood, Microsoft’s chief financial officer, told Wall Street that the on-premises Windows Server stack had a 3 percent revenue decline due to slower than expected Windows Server 2025 sales; support revenues followed suit. And looking ahead to Q3 F2025, Hood warned Wall Street to expect revenues for the on-premises Windows Server stack to “decline in the mid-single digits driven by a decrease in transactional purchasing.” And services revenues, while not declining, will sympathetically grow more slowly.

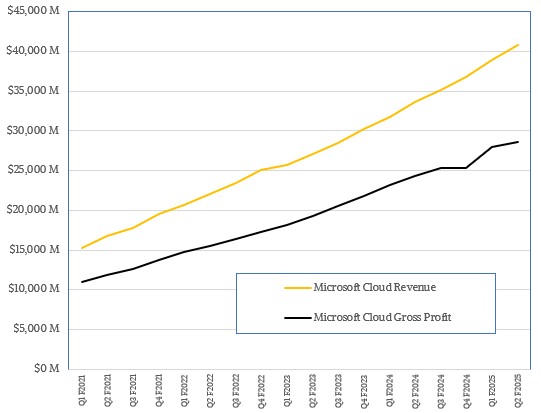

Now, every quarter when Microsoft does its numbers, we want to know two things, which it does not report on: What is its “real” overall systems revenue and profit, combining the Windows Server platform but not databases and development tools and other stuff with Azure capacity sales. And we also want to know how much revenue and profit Azure itself is driving, including all of the infrastructure, platform, and software services that ride atop it. The latter being something of a direct comparison to revenue and profit at Amazon Web Services.

We have spent some time doing spreadsheet magic to come up with these numbers. Let’s start with the latter, Azure.

In the second quarter, we reckon that Azure drove $15.79 billion in sales, up 31 percent as Microsoft said and representing 61.8 percent of revenues for the Intelligent Cloud group. Azure was half this size two years ago and was only 48 percent of Intelligent Cloud revenues. By our math, Azure had an operating income of $6.71 billion in Q2 F2025, up 25.4 percent year on year and representing 42.5 percent of revenues. Not quite Cisco-class, mind you, but those investments that Microsoft is making for the next decade and a half for datacenters are not cheap.

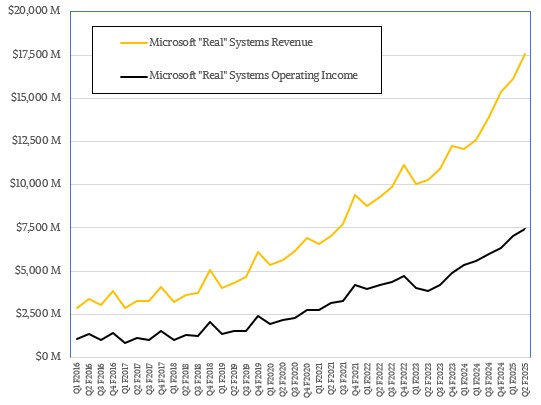

That brings us to the “real” Microsoft systems business:

Our model shows Microsoft generating $17.56 billion in revenue, up 39.2 percent year on year, for core infrastructure platforms, be they on premises or on Azure, and this further represents about 74 percent of the Server Products and Cloud Services revenues category that Microsoft does talk about. We think this “real” Microsoft systems business had an operating profit of $7.46 billion, up 25.4 percent.

A few thoughts. First, this whole business of the Stargate Project from OpenAI, where the AI model upstart is trying to build a coalition of partners to create massive datacenters to train AI models. This was the job of Microsoft Azure, right? Not anymore – at least not exclusively.

“As we shared last week we are thrilled OpenAI has made a new large Azure commitment,” Satya Nadella, Microsoft’s chief executive officer, said on the call with Wall Street. “Through our strategic partnership we continue to benefit mutually from each other’s growth. And with OpenAI’s APIs exclusively running on Azure, customers can count on us to get access to the world’s leading models. And OpenAI has a lot more coming soon, so stay tuned.”

Here is the other thing that was interesting on the AI front. That drop in the on-premises Windows Server stack transactions, tech support and other enterprise services, and Azure services other than AI were “partially offset by better than expected results in Azure AI services,” as Hood put it. AI services on the Azure cloud grew 157 percent year-over-year and “was ahead of expectations even as demand continued to be higher than our available capacity,” she said, adding that “growth in our non-AI services was slightly lower than expected due to go-to-market execution challenges, particularly with our customers that we primarily reach through our scale motions as we balance driving near-term non-AI consumption with AI growth.”

That sounds like the general purpose server recession caused by AI spending to us, a theme we have been expounding for nearly two years now.