While the hyperscalers and big cloud builders all are racing as fast as they can to build the biggest – and presumably the best – models, or collections of models, to win the AI race and become the Microsoft or Red Hat of commercial-grade models, the acquisition of AI hardware and envelope pushing on AI model architecture is not indicative of the adoption of AI by enterprises. Even if they have lots and lots of enterprises dabbling on their clouds.

If you want a litmus test for how pervasively AI is being adopted by large enterprises, perhaps Cisco Systems is the best test. With over 90,000 customers of its Universal Computing System converged server-switch hybrids worldwide and still the dominant market share of datacenter switching and routing, if Cisco is making money on AI systems, then it has gone mainstream.

The same cannot be said of Dell, Hewlett Packard Enterprise, or Lenovo, all of which have very established businesses selling compute, storage, and networking for more traditional HPC simulation and modeling. Supermicro has become one of the key suppliers of the hyperscalers and cloud builders for AI systems and has a relatively small presence in the enterprise proper. (But, a growing presence, mind you.)

And so, we watch Cisco very carefully to see transitions in enterprise computing as well as to see the adoption of AI among that fairly large and focused customer base that uses UCS iron for their mission critical applications.

Thus far, while we are impressed by the way Cisco is weaving AI into its products and also has acquired Splunk as a way to keep and sort through mountains of telemetry that can feed into AI systems for IT system management as well as into commercial applications, we are not yet seeing a significant pop in orders for AI systems, not at least compared to Cisco’s peers in the datacenter.

On a call going over the financial results for Cisco’s second quarter of fiscal 2025, a period that ended on January 25, Chuck Robbins, the company’s chief executive officer, and Scott Herren, its chief financial officer, reiterated that Cisco booked $1 billion in AI-related orders in fiscal 2024 (ended in July 2024) and further that it was on track to break through $1 billion in orders in fiscal 2025.

We think Robbins and Herren are low-balling the AI bookings forecast for 2025 – something we have seen from other IT vendors who are understandably cautious. (AMD, for instance, said it would do more than $2 billion in GPU sales in calendar 2024 and revised that many times up to $4.5 billion and then went in excess of $5 billion as last year ended.) We think the bookings rate accelerated through fiscal 2024. In fiscal 2025, Cisco has been more explicit, saying it did $347 million in bookings in Q1 and $355 million in Q2, and Robbins went even further to say that about half of that revenue this fiscal year was for merchant chips (we think mostly Silicon One switch chips) and systems. We think further that a lot of this is going into telcos and service providers who are building out their networks and infrastructure as they brace to add AI-enhanced applications and services.

Which brings us to the low-balling. With over $700 million in AI bookings so far in fiscal 2025, that only leaves $300 million to split across the remaining two quarters of the fiscal year. We do not think it is going down. In fact, it is far more likely to be growing. We think, based on the current trend in our AI booking model, that Cisco will probably do something between $1.6 billion and $1.7 billion in AI-related revenues. (And that is for components of AI systems, not for software and tools that are infused with AI, which Cisco is also selling.)

If Cisco can put a UCS twist on its GPU-accelerated systems (the Nexus HyperFabric AI clusters are UCS writ datacenter large, and were announced last June and are shipping now) and keep customers in the UCS fold as they add AI functionality, then we think there is no reason why Cisco cannot double its systems revenues, and further, see a much larger uptake of its Silicon One ASICs and switches based on them. This will, of course, take time, just like getting 90,000 UCS customers has taken a decade and a half.

And frankly it will happen as the AI focus moves from training to inference. Robbins said on the call that the opportunity for AI inference was “an order of magnitude higher” than what the world has seen with AI training.

In the meantime, Cisco has to sell what’s on the truck.

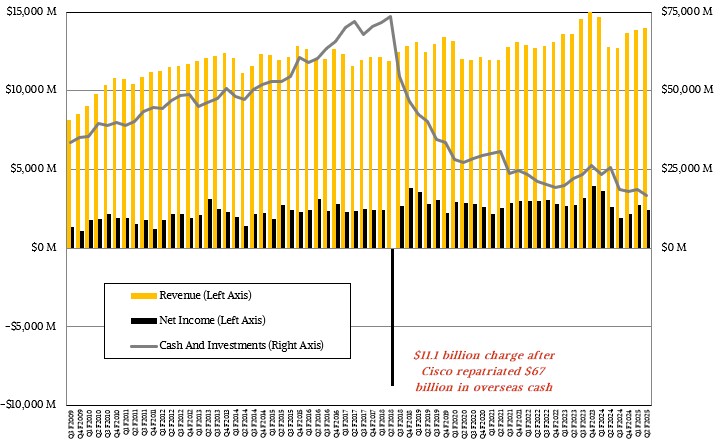

In the January quarter, Cisco’s revenues were $13.99 billion, up 9.4 percent year on year and up 1.1 percent sequentially. Costs rose faster than sales, however, and therefore net income dropped by 7.8 percent to $2.43 billion in the quarter. (Interest expenses were also quite a bit higher.)

Cisco ended the quarter with $16.85 billion in debt, down 34.4 percent from the year ago period and down 9.7 percent sequentially. Cisco has $11.41 billion in short-term debt and $19.63 billion in long-term debt, which is offset by the cash and $11.8 billion in deferred revenues.

In the quarter, services was relatively stable, as you can see in the chart above, growing 5.6 percent to $3.76 billion. Product sales, being transactional in nature still for the most part for Cisco, were up 10.9 percent to $10.23 billion.

Cisco’s networking products have been working off a huge backlog in recent years, and as you can see in the chart above, that backlog bubble is now gone and now Cisco is returning to a steady state of Networking sales that is just under $7 billion a quarter.

To be more precise, the company’s switching and routing products combined drive $6.85 billion in sales, down 3.3 percent, in the fiscal second quarter, but were up a smidgen sequentially. This Networking group is where server sales are also booked.

We have a model that stretches back to the Great Recession in fiscal 2009, which is also when the first generation “California” UCS converged server-switch systems launched and gave a heart attack to all of the incumbent server makers in the datacenter. And since that time, we have been trying to reckon what the “real” datacenter systems business revenue stream is from Cisco each quarter. Here is our best guess:

If you fill in the backlog hole from the coronavirus pandemic with the backlog bubble, this is a very steady business, indeed.

One Network Operating System To Rule Them All

Networks may not be the most expensive thing in the datacenter – they typically comprise about 10 percent to 15 percent of the cost of a distributed system, including cables, transceivers, switches, and routers – but they are without a doubt the most complex part of distributed systems. And anything …

AI Reshapes The Ethernet Datacenter Switch Market

Two decades ago, the hyperscalers and cloud builders started remaking the Ethernet switch market in the datacenter in their own image, and now it looks like AI training and inference is going to morph Ethernet switching in the datacenter once again. The amazing thing, as far as we are concerned, …

Ampere’s IPO Filing Signals More Arm Cash And More Arm Scrutiny

There is a likelihood that we could see both British chip designer Arm Holdings and one of its server-focused startup adherents, Ampere Computing, go public this year, as indicated by recent rumors of the first and news from Ampere itself this morning that it has confidentially filed for an initial …

Be the first to comment