Beleaguered chip maker Intel has been looking for ways to capitalize on non-core, not large, but profitable parts of its business to raise funds for its ambitious plans to revitalize Intel Foundry and to also invest heavily in the Intel Products group. And only two weeks after taking the helm of Intel, new chief executive officer Lip-Bu Tan is not wasting a lot of time getting things done.

To that end, Tan has engineered the sales of a 51 percent stake in Altera to private equity behemoth Silver Lake Partners for $4.46 billion, giving the FPGA maker a valuation of $8.75 billion. This is significantly less, of course, than the $16.7 billion that Intel paid to acquire Altera back in June 2015. (Which is more like $22.2 billion when you adjust for inflation to 2024 dollars, so Intel really only got about 20 percent of its money back out of the deal. Even if you add back in $2.63 billion in operating income that Altera contributed to Intel from the moment the deal was announced until the end of 2024 as an offset, Intel did not get a lot of its bait back when it went FPGA fishing.)

Intel started the process of spinning out Altera under prodigal son and former chief executive officer Pat Gelsinger, first separating out its financials in October 2023 and then early last year separating the company with its own books, management team, and budgets, naming Sandra Rivera as its chief executive officer and Shannon Poulin, a longtime Xeon CPU executive, as its chief operating officer. With the market for initial public offerings essentially dead at the moment due to the uncertainty on Wall Street and in geoecopolitics. Tan had little choice but to act now before the situation got worse. Intel needs to shore up its balance sheet, and sacrificing a controlling stake in Altera for $4.46 billion is a reasonable way to do that for some fast cash.

It is amazing, in fact, that Intel did not sell a full stake in Altera to Silver Lake or perhaps several private equity firms and hedge funds working in concert. Intel’s need for money to invest in its foundry business is that great. The stake it has sold is about a third to a quarter of the cost of a modern foundry, which is coming close to $20 billion depending on how you count the costs. So selling all of Altera to either Wall Street investors or to private equity firms must have been desirable.

It is not clear why Silver Lake bought the stake in Altera at all, but the company is not afraid to take a big stand with legacy IT suppliers. In February 2013, Michael Dell teamed up with Silver Lake and Microsoft to come up with $24 billion to take the company that bears his name private, and then when Dell needed $67 billion to buy EMC and VMware in October 2015, Silver Lake, MSD Capital, and Temasek lined up $4.25 billion plus another $50 billion in debt financial plus cash on hand from Dell, EMC, and VMware to do the deal, and when it was done, Michael Dell, Silver Lake, and Temasek ended up with around 70 percent of the controlling stock in the newly embiggened Dell. And a whole lot of debt that Dell, the company, is still paying off ever so slowly.

Perhaps Silver Lake has other reasons for wanting to help Intel out, and not any relating to Tan specifically.

Sometimes tech deals get done because they need to get done, and someone sitting in the White House helps make that happen. Bank of America bought Merrill Lynch for $50 billion in September 2008, as the toothy mouth of the Great Recession was opening wide, because someone had to help stabilize a very wobbly Wall Street and it had to be someone bigger than an investment bank, a hedge fund, or a private equity firm. And for an example that is closer to home, we have always thought that there was a political reason why supercomputer maker Cray ended up as part of Hewlett Packard Enterprise under a $1.3 billion acquisition deal announced in May 2019. Cray simply did not have a big enough balance sheet to take on exascale-class supercomputer deals. IBM was pretty much over losing money in HPC, and HPE needed a new story to tell, and had already acquired SGI back in August 2016. Dell has never had an appetite for capability-class supercomputing, and Lenovo, being half Chinese and half American, would never have gotten political approval of a Cray acquisition.

Silver Lake may have insisted that Intel keep quite a bit of skin in the FPGA game so that Intel Foundry would focus on keeping Altera as a customer for its chip fabbing operations. Intel has a vested interest in helping Altera make profitable chips on time because 49 percent of those profits will flow through to the Intel bottom line.

The best way to think about it, perhaps, is that Intel sold half a company to get half its profits but a quarter to a third of a foundry. And if you look at it that way, selling off Mobileye edge and consumer device AI accelerator business might get Intel the rest of a foundry.

Outstanding In Its Field (Programmable Gate Array)

To say that the Altera acquisition did not pan out as expected is an understatement. A lot of that failure has to do with Intel reading the market too aggressively for PGA acceleration in the datacenter and then not moving aggressively to compete against Xilinx, which was then acquired by AMD and which has in recent quarters been impacted by the same downturn in business that has hit Altera.

We don’t have much insight into Altera’s profitability at the net income level over the past nine years that Intel has owned it, but Altera had operating profits in 2024 but relatively severe net losses accompanying them. Before seeing the Intel statement, we surmised that this was probably due to writeoffs of inventory on hand, and if that is the case, it was a lot of inventory compared to the size of the company. It could also be for stock-based compensation, which would be needed to keep key employees in place. But it is not due to higher research, development, and sales costs, which come off the lines above the operating income level. But that is not to say that R&D and sales costs have not risen against slowing revenues to push operating profits down in 2023 and further in 2024. We think this happened as well. There were almost certainly restructuring costs that Intel offloaded to Altera as well.

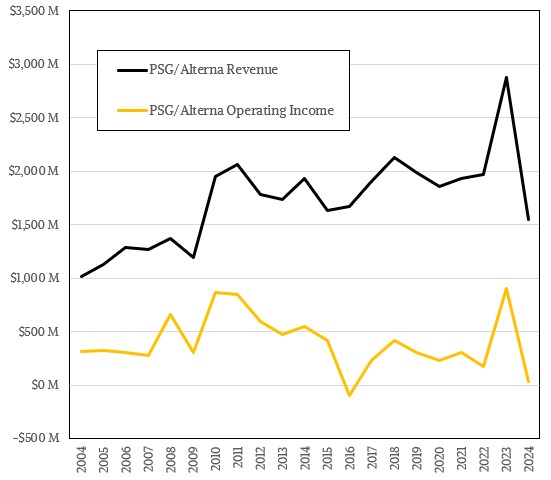

According to the statement put out by Intel announcing the takeover by Silver Lake, Altera had $1.54 billion in sales in 2024, but what Intel didn’t say was that sales had declined by 46.4 percent from the $2.88 billion in revenue that Intel posted with the Altera products in 2023. In recent years, Altera had around $2 billion in sales per year, and 2023 was clearly an anomaly and the decline in 2024 is just a leveling out after a bigger than usual bump in 2024. (Whether or not this was opportunistic and aggressive buying or channel stuffing is unknown.) Operating income was $903 million in 2023, way higher than usual for Altera. In 2024, operating income fell by 96.1 percent to $35 million on a non-GAAP basis. Using GAAP figures – the ones that count when it comes to paying taxes – Altera posted a $615 million operating loss in 2024, and its net loss was likely even deeper in the hole.

Clearly, if Intel wanted to take Altera public, sometime around February 2024 when the 2023 financials just came out would have been a great time. This is clearly not the case in early 2025, and probably would not have been in early 2026, either, the way the global economy is going.

Intel said further, as we paged down into the statement, that it had a gross margin of $361 million in 2024, and then $402 million in positive acquisition adjustments and $6 million in shared-based compensation adjustments (meaning reductions) that contributed to non-GAAP gross margins. That gave a non-GAAP gross margin of $769 million against that $1.54 billion in sales. Ah, but on a GAAP basis, Intel posted that $615 million operating loss, and then there were $491 million in acquisition related costs, $122 million in share-based compensation costs, and $37 million in restructuring costs, leaving an operating gain of $35 million.

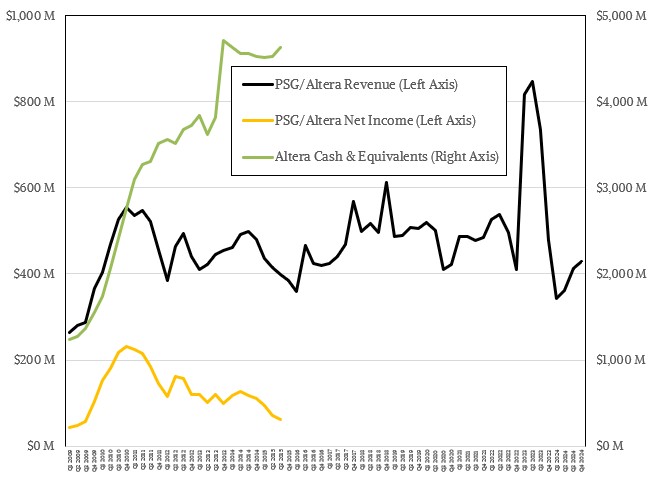

Here is a chart of quarterly revenue, net income, and cash that shows historical data for Altera from 2009 until 2015 when the company was independent and then adds revenue data going forward after the Intel deal went down. You can see how Altera’s revenue was choppy but more or less steady and net income was under pressure when the Intel bought it. Altera’s cash hoard never hit $1 billion, and probably was not going to the way sales were going and the way Xilinx was on the rise.

You can also see how the 2023 quarterly sales were an aberrant spike for three quarters. Go figure.

In the wake of the acquisition, Sandra Rivera, who spent a two and a half decade career at Intel, running its networking and datacenter groups and then eventually tapped to be the first chief executive officer of the spunout Altera, has been relieved of duty. She is replaced by Raghib Hussain, who was president at chip maker Marvell Technology until this week.

Hussain was chief technology officer and then chief operating officer at Cavium Networks, the chip startup that created the “Thunder” line of Arm server chips that eventually compelled Marvell to buy them to better compete with Intel. He has a bachelors in computer systems engineering from NED University of Engineering & Technology in Pakistan and a masters in computer engineering from San Jose State University. Hussain is on the board of directors for Cirrus Logic and Lightmatter and was the chief strategy officer for the Networking & Processors Group at Marvell from 2013 through 2021 before becoming president of products and technologies at the company.