For more than a year now, we have been talking about how investments in AI servers have put a damper on budgets for servers used to support other corporate applications. And we may be seeing enterprises pulling back on campus switching so they can invest more in datacenter switching to help cover their AI proof of concept and early deployment costs.

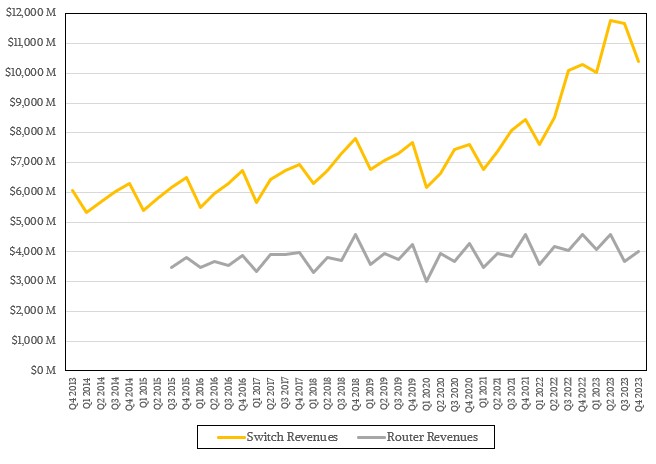

In the final quarter of 2023, worldwide sales of Ethernet switches rose by only eight-tenths of a point to $10.4 billion year on year from the fourth quarter of 2022, and fell by 11.1 percent sequentially from Q3 2023. There was a lot of activity in the Ethernet space in the second and third quarters of last year, and Q2 set a new peak at $11.8 billion in sales for datacenter, campus, and edge Ethernet switching combined.

Sales of routers, which have been under pressure for years as many Ethernet switch ASICs include routing functions, thereby allowing companies to build routers out of them instead of paying for expensive devices from Cisco Systems, Juniper Networks, Huawei Technologies, and a handful of other suppliers, had a 12.7 percent decline in Q4 2023, to just a tad over $4 billion.

For the full year, which is perhaps the best way to judge the switch and router markets given how boomy and busty sales into the hyperscalers and cloud builders can be, Ethernet switch sales rose by 20.1 percent to $43.9 billion, and we have a hunch – but we can’t prove it – that 2023 was the first year in the history of Ethernet that over 1 billion ports were shipped into the datacenter, the campus, and the edge.

Router revenues for 2023 were off four-tenths of a point to $16.4 billion. And frankly, given all of the pressure on routers, it is amazing that sales have been so stable over the past nine years for which data has been publicly available from IDC on this market.

Obviously, a huge gap has opened up between switching and routing revenues, which is ironic considering that, properly speaking, many of the hyperscalers and cloud builders are using switches with their routing functions and the BGP protocol to lash machines together in their giant 100,000 node Clos networks. This data is more about the main architecture of machines, and if we looked at ports by use case – switching or routing – then we might find that switching and routing revenues at least in the datacenter are closer than we might think.

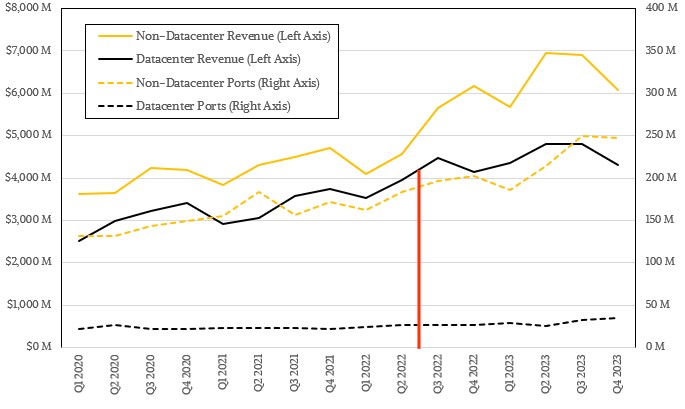

For the past several years, IDC has talked less about sales of switches and port counts by speed – which it used to do and which allowed us to build a very elegant model tracking port shipments and port costs by speed – and instead talks more generally about sales of datacenter and non-datacenter gear. We are, of course, happy to have this additional overlay on Ethernet switch data, but are of course saddened that the port speed segmentation is gone. IDC must have done some recasting of old data because based on what it now says, we no longer have confidence that we can fill in the gaps and give you a distribution of revenues and port counts by port speed. And to be honest, we think this data on port speeds and counts has been obfuscated specifically because we built a detailed model from it and told you about it.

IDC and Gartner have removed their quarterly server data from public view for the same reason.

So it goes.

What we can show you is the trend of spending on Ethernet switching in the datacenter and outside of it, and the port counts that IDC gave out (or that we could calculate from statements that it made) up until Q3 2022, when it put on the port count blinders. That blinder is designated by the red line below, and anything to the right of it when it comes to port counts is our estimate. Take a look:

Either way, Ethernet took a sequential dive in Q4 2023, and perhaps one that many Ethernet gear makers had not been expecting.

As best we can tell, datacenter Ethernet switch sales accounted for $4.3 billion in sales in Q3 2023 and made up 41.5 percent of overall Ethernet switch sales. That was a 10.1 percent sequential drop from Q3 2023 and down even further from the peak of $4.8 billion set in Q2 2023. We think that this revenue represented somewhere around 35 million ports shipped into the datacenter in the fourth quarter, which would be around a 35 percent growth rate in ports shipped year on year and about 10 percent sequentially. This is pretty good growth, especially considering that InfiniBand is having its day with AI server clusters (which IDC does not report on publicly.)

Sales of Ethernet switchery outside of the datacenter accounted for $6.1 billion in revenues, down 1.9 percent year on year and down closer to 12 percent sequentially; non-datacenter port shipments were probably somewhere around 250 million and up more like 22 percent. But again, that is just an educated guess.

Inside the datacenter, and as you might expect, sales of 200 Gb/sec and 400 Gb/sec Ethernet switches together rose by 68.9 percent for the full 2023 year and grew by 14.8 percent sequentially from Q3 2023. We think there is a very good chance that this category busted through $1.5 billion in sales for the quarter, possibly the third time sales have been above $1 billion.

What we can tell you with more certainty is that sales of 100 Gb/sec Ethernet switches in the datacenter keep humming along and growing modestly, and according to IDC accounted for 46.3 percent of the datacenter segment’s switching revenues. That means sales of 100 Gb/sec devices added up to $2.6 billion in Q4 and $10.5 billion for the full 2023 year, up 6.4 percent across the twelve months. That is the first time 100 Gb/sec switch revenues have surpassed $10 billion. It will take many, many years, but 100 Gb/sec is gradually replacing aging 10 Gb/sec devices in the enterprise.

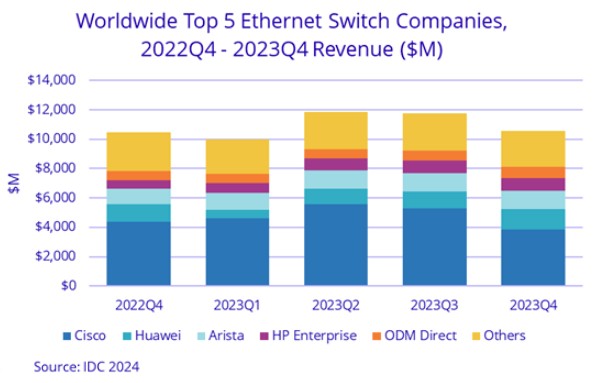

That brings us to the breakdown by vendor. Here is the chart IDC supplies:

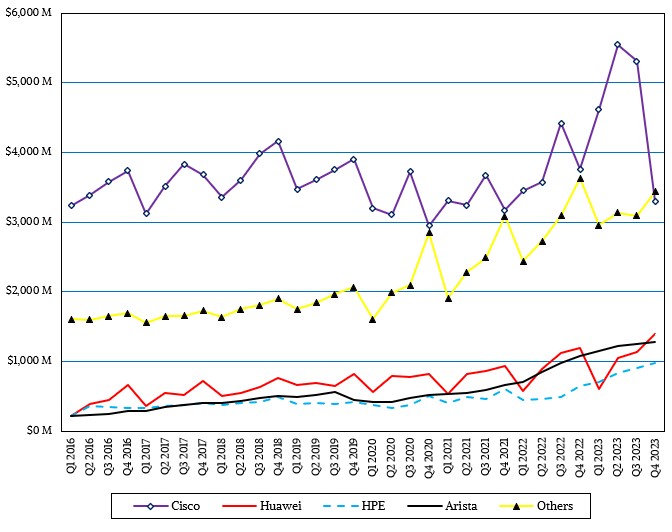

And here is one we create from the full historical dataset that gives you better trend perspective by vendor:

Cisco had a great second quarter and third quarter, but apparently took a nose dive in Ethernet switching in the fourth quarter, falling to about the same level as arch rival Arista Networks.

For the full 2023 year, Cisco’s Ethernet switch revenues across datacenter, campus, and edge uses was up 22.2 percent to $18.8 billion. More than two thirds of what Cisco sells is not in the datacenter. If you do the math based on what IDC said, Cisco had a little more than $1 billion in datacenter switch sales, but that was down 10.6 percent from the $1.13 billion in the year ago quarter and down 31.8 percent from the $1.48 billion we calculate Cisco had in Q3 2023. If you compare the trailing six months, revenues are up a tiny bit to $2.48 billion for Cisco in the datacenter.

Arista Networks had just under $4.9 billion in Ethernet switch sales across all segments, and as best we can figure, the company had a very good campus and edge showing in the first two quarters of 2023 and then its datacenter business accelerated even more, giving it $4.37 billion. In the trailing six months where we have hard data, Arista sold $2.31 billion in Ethernet gear into the datacenter – very nearly the $2.48 billion that Cisco did.

One thing: Isn’t it weird that in the past four years, Cisco and “the Others” have had virtually the same Ethernet revenues in the fourth calendar quarters?

Anyway. Thanks in large part to its success in HPC and AI supercomputing, Hewlett Packard Enterprise had $102 million in Ethernet switch sales into the datacenter in Q4 2023, up 39.6 percent sequentially from Q3, where it posted $73 million in sales. (The HPE Aruba products are largely sold in the campus and edge installations.)

According to IDC, the collective of original design manufacturer (ODM) switch makers that peddle gear into the datacenter comprised $643 million in sales in Q4 and $705 million in Q3 – we do not have any way to surmise data from Q1 and Q2. But we do know that overall ODM switch sales for 2023 were $2.61 billion, and growing. ODM makers now account for 14.3 percent of datacenter segment Ethernet switch revenues in 2023 and grew 16.2 percent year on year from 2022.

At this rate, with the ODMs growing only a few points faster than the overall market, it will take a long time for the ODMs to account for the same representative share in switches as they currently have in servers in the datacenter. But there is no reason to believe that the same economic forces will not be at work in switching as have been on servers and storage. It just took a while longer.

Those who can ODM – or make their OEM behave like an ODM for them – will. And those who cannot – meaning the vast majority of enterprises, government agencies, and educational and research institutions – will pay the enterprise premium for their Ethernet switching in the datacenter.

This 15 percent share that the ODMs have attained as last year came to a close is just the beginning.

You can load a hyperscaler operating system on a switch made by Supermicro just as easily as you can on one made by Arista, and we have a pretty safe bet on which on is cheaper. And if Supermicro is making your rackscale AI and web infrastructure systems, why wouldn’t you just let Supermicro build and support the switches, too?

This is but one example. What is true of Ethernet is also true of InfiniBand. Why not use an ODM switch based on InfiniBand if you need it, and trim some of those Nvidia profits out of your budget?

Can Nvidia Be The Biggest Chip Maker In The Datacenter?

Next year, with the launch of the “Grace” Arm server processors, Nvidia will have all of the compute and networking bases it cares about in the datacenter covered, and it will be selling its technology at a rapid pace. Nvidia already has a larger datacenter business than AMD has – …

A Bumper Crop Of Ethernet Switches Harvested In Q4

With each passing year, the phrase “The network is the computer,” coined in 1984 by John Gage, director of research and co-founder of Sun Microsystems, becomes more and more true. And it was certainly at its most truest in 2022 if you use Ethernet datacenter switching revenues as a gauge. …

The Slow But Tectonic Shifts In Datacenter Infrastructure

One of the more interesting trends in infrastructure that we try to get a handle on every once in a while is how much of the server and storage capacity is being deployed in bare metal, standalone fashion and how much is being sold to run utility style, cloud environments. …

Excuse me fan tech boys, UltraEthernet tech (consortium)is now in cooking stage, I think soon to surge Therab/s, that specifications interconnection it is in developing route (next, middle this year 2024)

“Why not use an ODM switch based on InfiniBand”

Who will sell the Silicon to the ODM ?

Cornelis Networks, for one. Nvidia will, too. Question is: At what price?

I think this just shows the widening gap between the people who run stuff at scale, and those poor shmucks who have to roll their own. I’m including businesses with tight fisted management who don’t want to spend money on “extras”, etc. The hyperscalers can do the math and figure out that spending up front on IPMI and other services, and automation has paybacks. And that allows them to push back on the Ciscos on price and/or get ODMs to build to their specs so their scaling keeps on going.

It’s like comparing a family farm to one of the 2000+ acre farms in the American west. Just a totally different level of scale and needs and ability to spend to save money over the longer haul.

Now how do we get those scaling advantages down into the smaller shops? And how do you get away from the entrenched “I know Cisco, so that’s what I use” mindset as well?

And you have a typo in there as well: “the BGP protocol to last machines together” which probably should be “lash” instead.

Could not agree more. There is a bifurcation that is insurmountable. The hyperscalers and cloud builders had money at scale and then infrastructure at scale, and now they have performance at scale. A normal enterprise is limited by money, capacity, and now performance. It all comes down to money, don’t it?