Just because you are the number one supplier of servers, storage, and PCs in the world does not mean the job of building those machines and making money is easy. It is not, and the financials of Dell Technologies shows just how tough it can be even when things are improving. Even the GenAI boom is not a cut and dry positive because of the cost and complexity of building large numbers of supercomputers.

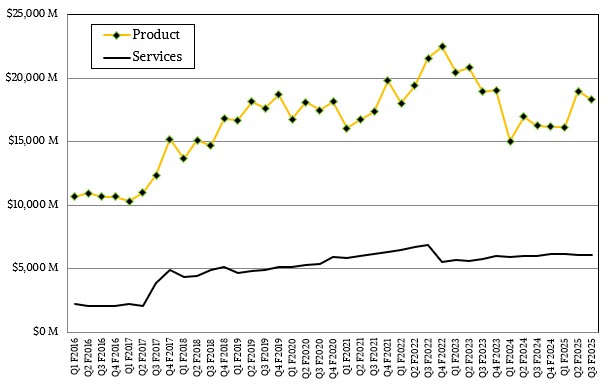

In the quarter ended on November 1, which was the end of Dell’s third quarter of its fiscal 2025 year, the company posted product sales of $18.29 billion, up 12.7 percent year on year but down 3.5 percent sequentially, with services spending limping along at $6.08 billion, up a mere point year on year and up a tiny smidgen sequentially.

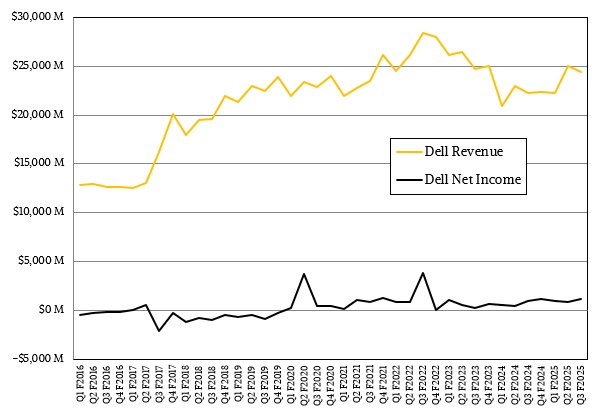

Add it all up, Dell’s overall revenues rose by 9.5 percent to $24.37 billion, with operating income rising 12.2 percent to $1.67 billion and thanks to the typical Dell cost cutting, the company was able to boost net income by 12.3 percent to $1.13 billion. That net income represents 4.6 percent of revenues, which is a tiny bit higher than the average of 4.3 percent across the prior four quarters and better than the 3.9 percent average since the beginning of fiscal 2020.

That Dell can generate a billion dollars a quarter in profits the cut-throat markets it participates in is a testament to the cost-cutting mentality that led Michael Dell to get into the PC business four decades ago. We never forget this, and as we are fond of pointing this out, someone needs to build the machinery we need and, these days for sure, we prefer for that company to be located in North America with a strong European presence rather than being located in China. We never know when a real trade war might erupt, and a distributed supply chain is a good thing given this.

Everybody has been watching Dell’s traditional and AI server businesses like a hawk, and Wall Street is not thrilled that Dell has lowered its forecast for AI server spending in the final quarter of fiscal 2025, saying that it expected a slight sequential decline instead of growth. But the good news is that customers have been doing precisely what we have been advising for the past several years: Buying servers with fat CPUs to upgrade their server farms and get rid of fleets of old machines that burn too much power, giving their datacenter space as well as power and cooling to build modest AI server clusters to support GenAI workloads.

“Traditional servers demand improved and customers are buying more richly configured servers, which we have seen over the last few quarters,” Yvonne McGill, Dell’s chief financial officer, said on a call with Wall Street analysts going over the Q3 F2025 numbers. “Units and ASPs grew with denser core counts and more memory and storage per server. So again, great to see. Customers focused on consolidation and power efficiency by modernizing their data centers, which frees up some volume or space for AI infrastructure. From an AI standpoint, AI servers as well as storage margins were flat to slightly up quarter-on-quarter, so that was again good to see. And we also realized more cost efficiencies quarter-on-quarter helping our operating income. Looking into Q4, expect ISG operating income rates to continue to improve.”

It is good to see that server margins are improving, but we think that has more to do with companies buying fat servers than it does buying AI servers. Remember: AI is accretive to operating income dollars but not to operating income share of revenue at Dell.

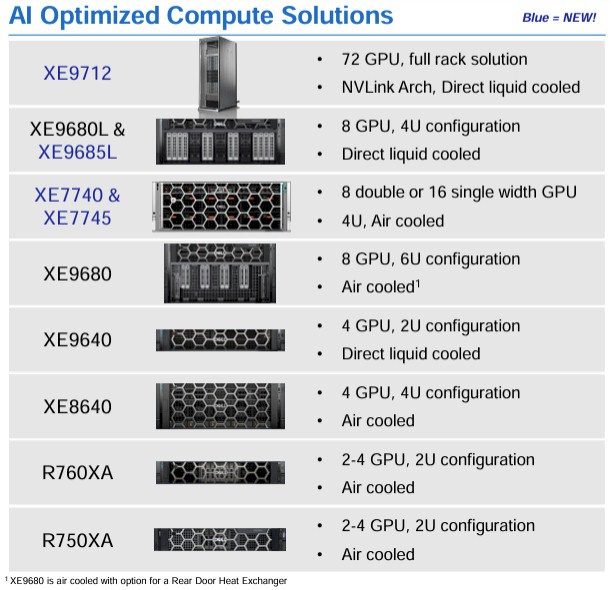

On the AI server front, Dell is rolling out a wide variety of server platforms to try to capture the GenAI opportunity in the enterprise:

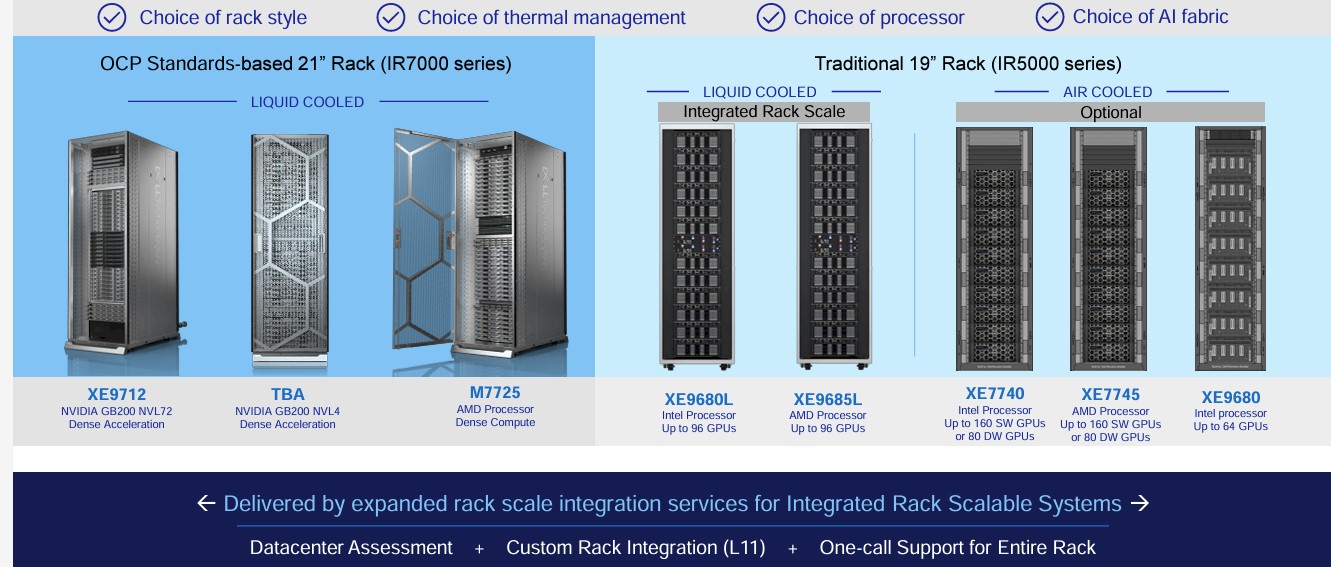

And that also means Dell needs a wide variety of ready-to-go, rackscale systems on which to build AI supercomputers:

It is interesting to note that both Hewlett Packard Enterprise and Dell are using AMD’s “Turin” Epyc server CPUs as their CPU-only choice for packing more X86 performance into a rack.

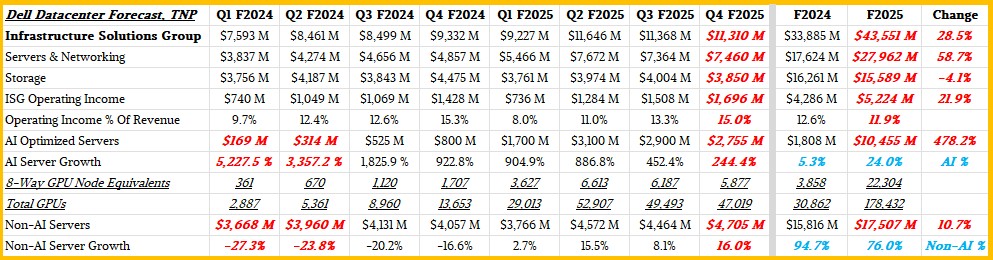

In the quarter, Dell’s Infrastructure Solutions Group had $7.36 billion in server and networking storage, up 58.2 percent year on year but down 4 percent sequentially. Storage sales were up 4.2 percent to just a tad over $4 billion in Q3 F2025, and up a smidgen from Q2. Add it all up, ISG had $11.37 billion in sales, up 33.8 percent but down 2.4 percent sequentially.

The good news is that operating income was up a stunning 41.1 percent and up 17.4 percent sequentially. This can be credited to the use of high bin CPUs from Intel and AMD amongst large enterprises who are cramped for space and power in their datacenters.

In the quarter, Dell said it sold $2.9 billion in AI servers, which we presume also includes any networking associated with those clusters, which was up by a factor of 5.5X compared to the prior year’s period, but alarmingly was down 6.5 percent sequentially.

Jeff Clarke, Dell’s vice chairman and chief operating officer, said that customers had started to shift away from Nvidia “Hopper” GPUs and towards “Blackwell” GPUs, which is another way of saying that customers are willing to wait for a better product with better bang for the buck for AI workloads than just take older Hopper units at this point. (That’s what we would do, especially given the cost of these AI beasts.) The $4.5 billion backlog in AI server sales at Dell as it exited Q3 F2025 is significantly represented by customers waiting for Blackwell systems. That backlog is up by a factor of 3X compared to a year ago and is up 18.4 percent sequentially.

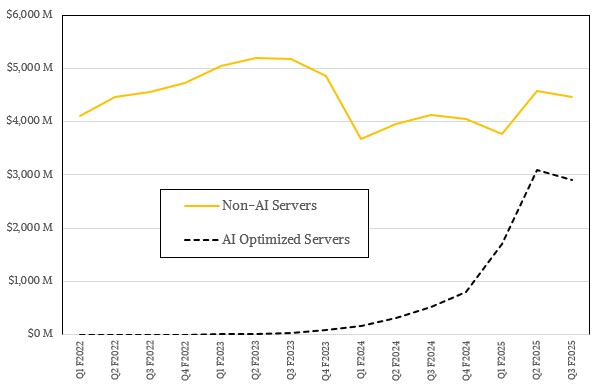

Even with the high bin bump in traditional server spending, if you do the math, this means non-AI server spending was $4.46 billion, up 8.1 percent but down 2.5 percent sequentially. We think that SMB server sales might be flat or down, but that is a hunch not based on data.

The fact is, server spending is cooling, as the chart above shows.

Based on what Dell said on the call, here is our updated forecast for Dell datacenter sales for fiscal 2025:

Dell will sell around $10.5 billion in AI servers this fiscal year, if our guess about Q4 F2025 are right, which is a factor of 5.8X higher than in fiscal 2024. This is a huge increase, obviously, and is a testament to the GenAI boom. But as our table shows, Dell is not moving a huge number of GPUs to make that money. This is only the beginning of the mainstreaming of GenAI. When that happens, more than half of Dell’s revenues will be driven by AI servers, whereas it will be about 24 percent of sales in fiscal 2025.

Depending on how the economy goes, it is probably a safe bet that that 50 percent crossover for AI servers will happen in late fiscal 2026 or maybe early fiscal 2027. We have no doubt at all that this will happen for HPE as well, perhaps sooner given its exascale supercomputer installations.

One Way To Bring DPU Acceleration To Supercomputing

That is not a typo in the title. We did not mean to say GPU in title above, or even make a joke that in hybrid CPU_GPU systems, the CPU is more of a serial processing accelerator with a giant slow DDR4 cache for GPUs in hybrid supercomputers these days …

Nvidia Lays The Foundation For Wider AI Adoption

For a decade and a half, Nvidia has been pushed its way into the datacenter, making its presence felt with its GPU accelerators that are designed to improve the performance and power efficiency of servers in HPC and enterprise compute environments and also expanding the opportunities for running highly parallel …

VMware Embraces Nvidia GPUs, DPUs To Drive Enterprise AI

AI is too hard for most enterprises to adopt, just like HPC was and continues to be. The search for “easy AI” – solutions that will reduce the costs and complexities associated with AI and fuel wider use by mainstream organizations – has included the development of myriad open source …

Be the first to comment