Nvidia may be shipping its “Blackwell” B100, B200, and GB200 compute engines, but not in enough volumes for server maker Supermicro to meet its revenue expectations in the quarter ended in December. And the less-steep Blackwell ramp has put a damper on the next two quarters as well, the companies top brass said on a call going over preliminary financial results for its second quarter of fiscal 2025.

The financial drama surrounding Supermicro’s accounting is coming to a close, company founder and chairman Charles Liang said on the call with Wall Street, explaining that Supermicro would file full and audited financials for its fourth quarter of fiscal 2024 as well as the two completed quarters of fiscal 2025 by February 25. We will update our financial analysis when the audited financials come out, but in the meantime, we have put together some trend data based on the preliminary financials using the midpoints of estimated made in the first half of fiscal 2025.

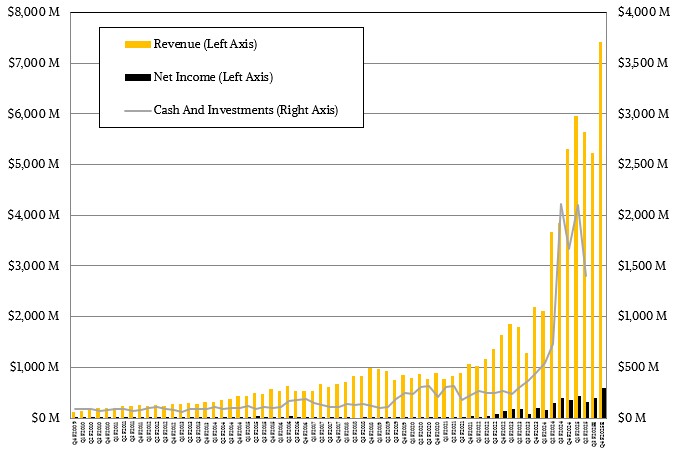

Let’s start with what we know. In the quarter ended in December, Supermicro said that its overall sales were between $5.6 billion and $5.7 billion, and at the midpoint of that pretty tight range, that means they rose by around 54 percent compared to the year ago period. Net income on a GAAP basis is expected to be in the range of $315 million to $325 million, and at the midpoint that will be 8.1 percent higher than the year ago period and only representing around 5.7 percent of revenues.

Because so much of the product mix sold in Q2 F2025 was apparently based on “Hopper” H200 accelerators and not Blackwell B100 and B200 devices, or the GB200 pairing of the “Grace” Arm server CPU and the Blackwell GPU, Supermicro’s profitability clearly took a hit. The company danced around calling out Nvidia directly for the revenue miss and profit decline, as you might imagine it would as it awaits its next B100 and B200 GPU allocations.

When asked directly how much of the revision in the fiscal 2025 forecast was due to the change in auditors and the lack of audited financials for Q1 and Q2 of this fiscal year or to delays in the ramp of the Blackwell CPUs, Supermicro’s chief financial officer, David Weigand, was clear.

“Probably the biggest factor was just the delay in new technology because we were, when you think about it, we were all set to go,” Weigand explained. “We were all set to ship with liquid cooling. We were ready. But the problem was that not everything else was. So that was certainly a huge impact. I think, obviously, the 10-K delay was a distraction. But it’s more about technology for us, because we count on being early to market.”

But Blackwell is now shipping and ramping, and that is a chance to drive more sales and extract more profits, according to Liang, who said that new technology always presents a chance to extract more profits, and this is particularly true as Supermicro is moving from rackscale systems to full cluster installations, including direct liquid cooling on machinery and the chillers for the datacenters that house its AI systems.

Liang said on the call that more than 70 percent of Supermicro’s revenues in Q2 F2025 were for AI systems, which is consistent with the levels we saw in the prior two quarters. Our model shows AI systems accounting for 72 percent of revenues, to $3.93 billion, and that non-AI systems (not including the motherboard and component business that Supermicro still has) accounted for just over $1 billion in sales.

As you can see, our model shows Supermicro having an underlying systems business that has been humming along at around $1 billion a quarter since the GenAI boom started, and its fledgling AI business from two years ago has now grown by more than an order of magnitude over that time.

And based on projections that Supermicro offered for future revenues in fiscal 2025 and 2026, it looks like the AI boom, which slowed a bit in recent quarters as Blackwell ramped more slowly than expected, is going to regain momentum.

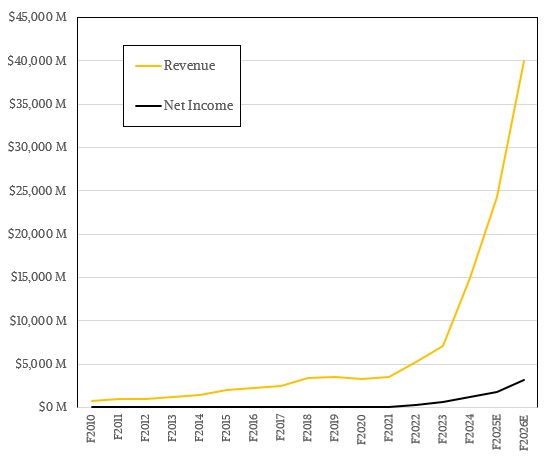

On the call, Liang said that Supermicro expected to have between $23.5 billion and $25 billion in overall revenues in fiscal 2025. That is down significantly from the $26 billion to $30 billion range that Supermicro had previously predicted, wiping out anywhere from $1 billion to $6.5 billion in revenues, depending on how this all plays out. (It’s close to $3 billion at the midpoints.) At the midpoint of that updated revenue for F2025, the math shows around $12.65 billion in revenues left to be raked in during 2H F2025. For Q3, Supermicro says expect sales between $5 billion and $6 billion, which is a pretty wide range and shows the lingering uncertainty in the allocations for Blackwell GPUs from Nvidia.

Our guess is Supermicro will have $5.24 billion in sales in Q3 and $7.41 billion in Q4, which gives Nvidia more time for the full-on Blackwell blitz. We think Supermicro’s profitability will rise as the fiscal year goes on, not so much because Blackwells are inherently more profitable for Supermicro but because Supermicro has a much bigger slice of the AI datacenter revenue stream, including preconfiguring hardware and software at a cluster level as well as datacenter cooling systems.

Looking ahead for fiscal 2026, which will start in July and run through next June, Liang said that a “conservative estimate” for Supermicro’s growth is 65 percent year on year, to at least $40 billion in sales.

A company buying so many GPUs and other parts to sell complete systems needs a lot of cash to do its work. Supermicro had $2.1 billion in cash when it started fiscal Q2, but by the end of it, even with its profits, after paying off some debts, buying shares for employee compensation, and buying parts for system deals, the company exited the quarter with only $1.4 billion. That is a much larger cash hoard than Supermicro ever used to carry, but it is not a lot for a $30 billion or $40 billion manufacturer of the HPC systems. (This deep pockets problem is why Hewlett Packard Enterprise had to buy Cray.)

To that end, Supermicro has raised $700 million through senior convertible notes that are paying out at 2.25 percent. Supermicro previously raised $1.5 billion through senior convertible notes back in February 2024. This debt can be paid back, rolled over, or converted into shares at a predetermined rate. The notes from February were set at a 37.5 percent premium over the then-current price of Supermicro shares, and the ones priced this week are set at a 50 percent premium. We won’t be surprised if Supermicro goes back again for more notes from its investors.

Supermicro knows it has to make it up in volume, and that means having a big and strong balance sheet or it can’t do the big deals.

The thing that Liang and Co know is that if they can keep up this pace, there is a chance to topple Dell as the world’s largest server maker and probably with somewhere between 2X and 3X the AI system sales.

DOE AI Expert Says New HPC Architecture Is Needed

Artificial intelligence is taking center stage in the IT industry, fueled by the massive growth in the data being generated and the increasing need in HPC and mainstream enterprises for capabilities ranging from analytics and automation. AI and machine learning address a lot of the demands coming from IT. Given …

Marvell Pivots To AI Silicon, Looks Poised To Profit

It is hard to bet against the GenAI boom, and thus far it is also hard for anyone other than Nvidia to profit from it. No one knows these facts better than Marvell Technology, who along with rival chip maker Broadcom, is seeking to benefit from the bevy of custom …

AMD Firing On All Compute Engine Cylinders

A few years ago, it was hard to imagine how AMD would have survived without re-entering the datacenter with its CPU and GPU compute engines. And now, it is hard to imagine how the chip maker could have possibly thrived without a revitalized GPU compute engine business. Intel knows a …

Perhaps it should be called the Blackwhere GPU?