Two decades ago, the hyperscalers and cloud builders started remaking the Ethernet switch market in the datacenter in their own image, and now it looks like AI training and inference is going to morph Ethernet switching in the datacenter once again.

The amazing thing, as far as we are concerned, is how much campus and edge switching drives the overall Ethernet market. But as we have pointed out in recent quarters, we think that enterprises, governments, as well as all kinds of service providers have been stalling their spending on campus and edge gear so they can invest in networking equipment for their AI systems. This has happened with server spending for sure, as we have shown, causing a recession in general purpose server spending. (That general purpose server recession is now over as companies finally need to upgrade their old servers to save power and cooling for AI systems.)

Massive order backlogs hanging over from the coronavirus pandemic significantly boosted Ethernet switch sales in 2023 among campus and edge gear, and sales in 2024 had some tough compares. The datacenter portion of the Ethernet switch market, based on our interpretation of data released by IDC that we have been curating for years, dipped at the end of 2023 and into early 2024, but have resumed their growth in large part thanks to AI clusters and, we think, in large part because of the large deals that Nvidia has taken down for its Spectrum-X Ethernet gear. (More on this in a moment.)

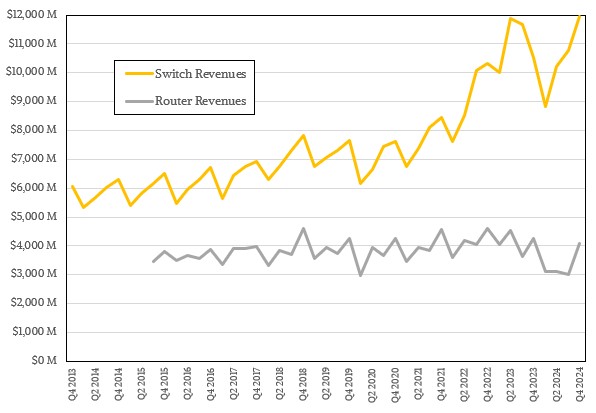

In the fourth quarter, IDC reckons that just under $12 billion in Ethernet switching equipment was sold in the fourth quarter of 2024, an increase of 13.3 percent over the year ago period. Ethernet router sales, which tend to bumble along steadily with some wiggling up and down, were off 4.5 percent to $4.08 billion based on our interpretations of the sparse IDC data, which nonetheless allows us to work the math around to get a sales figure of reasonable precision.

For the full year, it looks like Ethernet switch sales were off by 5.4 percent to $41.78 billion and Ethernet router sales dropped by 19.1 percent to $13.32 billion.

IDC used to give out revenue growth and port shipment growth for multiple bands of Ethernet switching, but its publicly released data no longer offers this granularity. It has been many quarters since this data was pulled, and as time passes, we are less and less comfortable with any estimates we make based on Ethernet switch shipments based on port speeds.

The market researcher did say that revenues for Ethernet switches with 200 Gb/sec and 400 Gb/sec ports rose by 147.5 percent compared to the year ago period and were up 25.9 percent sequentially from Q3 2024. These machines are only used in the datacenter, not on the campus or at the edge. This growth was no doubt driven by the use of Ethernet switches, largely from Nvidia, for AI clusters. There is, we think, some uptick in spending on 400 Gb/sec gear by hyperscalers and cloud builders and the beginnings of a ramp for 800 Gb/sec gear, too.

When we do the math on that based on a model we built for many years, we think datacenter Ethernet switch revenues overall were $5.78 billion, compared to $4.38 billion in Q4 2023 and to $5.39 billion in Q3 2024. That means datacenter Ethernet switch revenues comprised 48.4 percent of overall Ethernet switch revenues in the period.

We estimate, based on what IDC has said in the past and some educated guessing, that datacenter Ethernet switches accounted for 14.2 percent of ports shipped in the December 2024 quarter, a little higher than usual and driven no doubt by AI system installations and more than a few HPC systems using Hewlett Packard Enterprise’s “Rosetta” Slingshot interconnect, which is a variant of Ethernet.

In the chart above, any port count data that is to the right of the vertical red line are our estimates, not IDC’s. The revenue data for datacenter and non-datacenter Ethernet switches is our estimate based on what limited data IDC does give out, which does allow you to make some pretty good guesses.

Here is the vendor chart that IDC puts out for the Ethernet switching market, which highlights the five prior quarters of data and shows revenue shares for Cisco Systems, Arista Networks, Huawei Technologies, HPE, the ODM collective, and Others:

We like longer datasets than this, and so we present you with this alternative, which allows for you to better see how each vendor or group of vendors is doing.

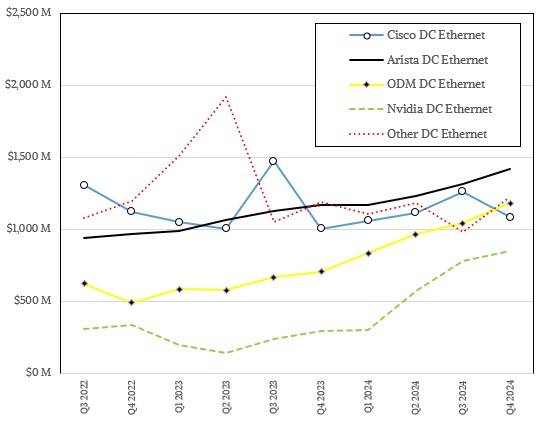

While this chart is interesting, we care about the datacenter. Luckily, for the past two years, we have been tracking the little breadcrumbs that IDC analysts have been giving out about the portion of the business the top five vendors have that come from datacenter Ethernet switch sales. And now we have enough data to present a few years of trends for vendors who sell into the datacenter:

Because Nvidia does not sell Ethernet campus and edge switches, it does not rank among the top four plus the ODMs grouping and Others that IDC uses in its charts. But Nvidia is most certainly part of the Others, as is H3C, Juniper Networks, Extreme Networks, Dell, and a slew of others who dabble in Ethernet switching. But we think that the increasing number of customers building very large AI clusters based on Ethernet interconnects and Nvidia GPUs will actually make Nvidia a player in datacenter Ethernet. Perhaps the dominant one in terms of revenues at some point in the not-too-distant future.

And to prove the point, we normalized Nvidia’s sales for calendar years and then plotted our estimates of Ethernet switching revenues from our Nvidia model into the IDC vendor model. Which you can see in the dashed green line above.

This Nvidia revenue in our model for the company includes DPU and SmartNIC revenues as well as switches for both InfiniBand and Spectrum gear. Our best guess is that the switches account for 65 percent of the hardware cost and the SmartNICs and DPUs account for 35 percent, so we have adjusted to extract the server endpoints from the Nvidia revenues to get something that is probably close to a pure switching revenue number.

It is hard to forecast how much money the Spectrum-X switch business will rake in for Nvidia. Our conservative model shows that Nvidia can catch Cisco Systems in datacenter switching revenue (for much different classes of customers with a little AI overlap perhaps) in a little more than a year, provided Cisco stays around $4.5 billion a year.

Cisco is partnering with Nvidia for precisely this reason.

Our model for Nvidia datacenter Ethernet switching has the company making $890 million in sales in calendar 2023, and growing by 2.8X to $2.51 billion in calendar 2024. For calendar 2025, we see a minimum of around 67 percent growth annually and sequential growth each quarter for all of the 2025 year, for around $4.2 billion when it is all added up. (Remember, this is just revenue for Spectrum switches, not the SmartNICs, DPUs, or cables.) Assuming that prices moderate because of competition and the network starts representing a smaller portion of the AI cluster cost, we think a minimum of 21 percent growth in calendar 2026 is logical for Nvidia’s Spectrum switch business, which puts it at $5.1 billion or so.

It can get much bigger, much faster, but the curve about doesn’t show that so far. It shows Nvidia more or less tracking Arista, but about two years behind it.

So catching Arista Networks will be much harder for Nvidia. That company had $5.15 billion in datacenter Ethernet switch sales in 2024, up 18.1 percent from 2023’s $4.36 billion. Assume as a bare minimum, and that the AI segment does not implode under the weight of its own lofty expectations, that Arista Networks can grow its datacenter Ethernet switch business – this is just hardware, not software and services – by 20 percent this year and then 15 percent annually after that. So it might hit $6.2 billion in for datacenter switching in 2025, $6.9 billion in 2026, $7.7 billion in 2027, and $8.6 billion by 2029.

It will be fun to watch this battle.

Datacenter Becomes Nvidia’s Largest Business

Something that we have been waiting for a decade and a half to see has just happened: The datacenter is now the biggest business at Nvidia. Bigger even than the gaming business for which it was founded almost three decades ago. The rise of the datacenter business has been no …

Lawrence Livermore To Surpass 2 Exaflops With AMD Compute

As the steward of the nuclear weapon arsenal for the United States government, it is probably not an overstatement to say that Lawrence Livermore National Laboratory, one of the main supercomputer and scientific research facilities operated by the Department of Energy, is keenly interested in bang for the buck. And …

The HBM3 Roadmap Is Just Getting Started

To a certain extent, the only thing that really matters in a computing system is what changes in its memory, and to that extent, this is what makes computers like us. All of the computing capacity in the world, or the type of manipulation or transformation of that data, doesn’t …

Be the first to comment