It would be hard to pick a worse time to not have an XPU offload engine that can do lots of matrix math at mixed precision and that can ship in volume. But this is precisely where Intel finds itself as there is a server recession in the datacenter. And this, along with the difficulties of cleaning up its mess in chip manufacturing, is weighing down Intel’s financial results like Jovian gravity.

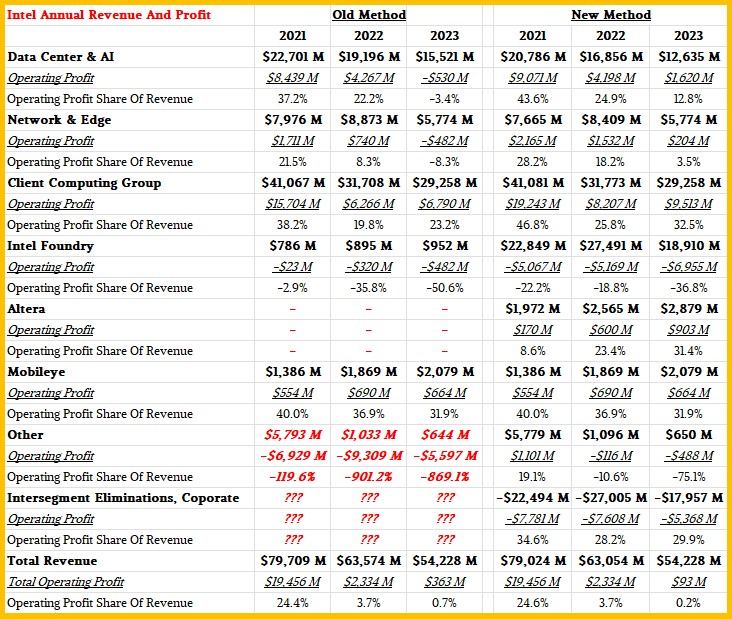

Earlier this month, we got some insight into Intel’s true financial health when it rejiggered its annual books for 2021, 2022, and 2023 to include its product groups paying the Intel Foundry business for chip etching and packaging services, just as if they were an outside customer like Microsoft and a handful of others who are signing up to use the company’s future 18A and we presume 14A processes. People are not just excited that Intel has opened up its fabs to outside business. They are trying to mitigate the risks of having all of the world’s chips coming out of one basket called Taiwan Semiconductor Manufacturing Co, which is having a tough time with earthquakes in recent weeks and is always under a threat of invasion by China.

Intel thinks is can be the second largest merchant foundry in the world by 2030, which seems likely enough, but as we pointed out in going over TSMC’s financials more recently, even should Intel get to the $40 billion in overall revenues that its forecasts suggest are possible – $15 billion of that from outside customers – TSMC will have an AI accelerator etching and packaging business that itself is larger than Intel’s foundry biz. Top be more specific, as we showed in our model, if TSMC grows faster than average in the next couple of years and then slows down lower than average in the couple of years after that, it will have around $178 billion in sales in 2030.

So yes, Intel can be number two. But TSMC will, unless something radical changes, be 4.5X as large as Intel Foundry.

Yikes.

The good news for the Intel product groups is that their profit and loss statements have been backcast three years and recast for Q1 2024 so that they pay only market rates for foundry services from their sister foundry operation. Which has the immediate effect of making these product groups more profitable than they looked in the past. In fact, the change in bookkeeping has wiped out some embarrassing operating losses in the “real” datacenter business at Intel, by which we mean the sum of the Data Center and AI (DCAI) group, the Network and Edge (NEX) group, and the newly spun out Altera FPGA business.

Look for yourself, no more red ink:

Admittedly, operating income is pretty low there in Q3 2022, as you can see. But look at all of that money Intel made – by which we mean operating profits – between the end of the Great Recession and the beginning of coronavirus pandemic, which coincided with the rise of AMD in CPUs and the absolute dominance of Nvidia in GPUs.

Just for reference, here is the annual recasting of Intel’s results, showing the old and new ways of counting the beans:

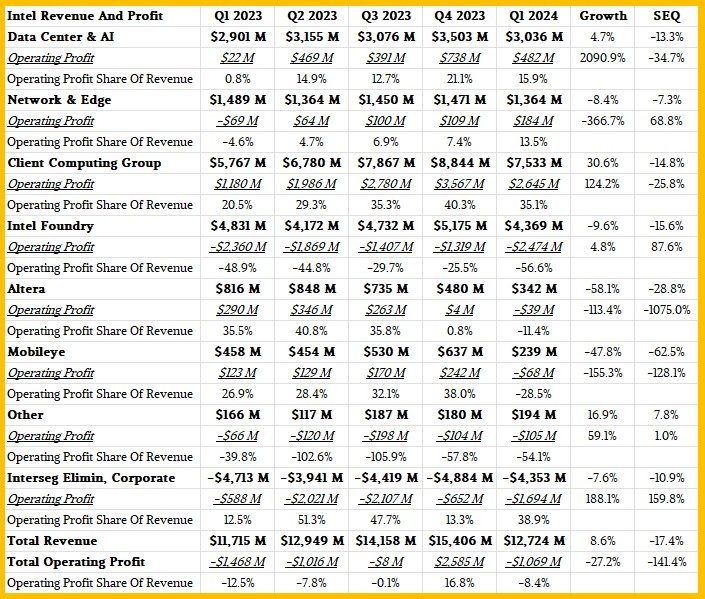

And here is an updated table showing quarterly results for the past five quarters:

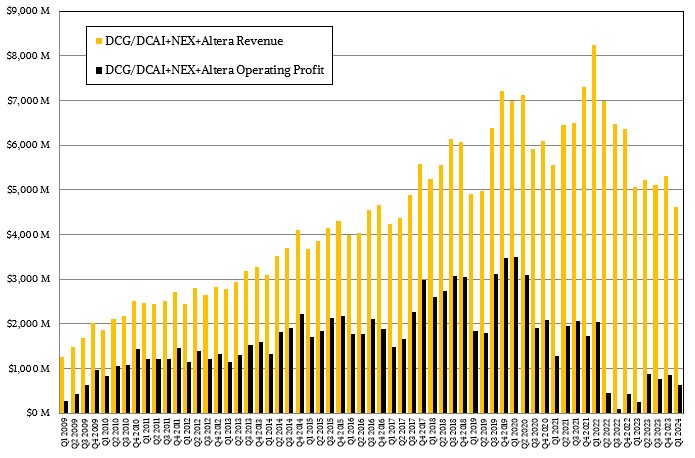

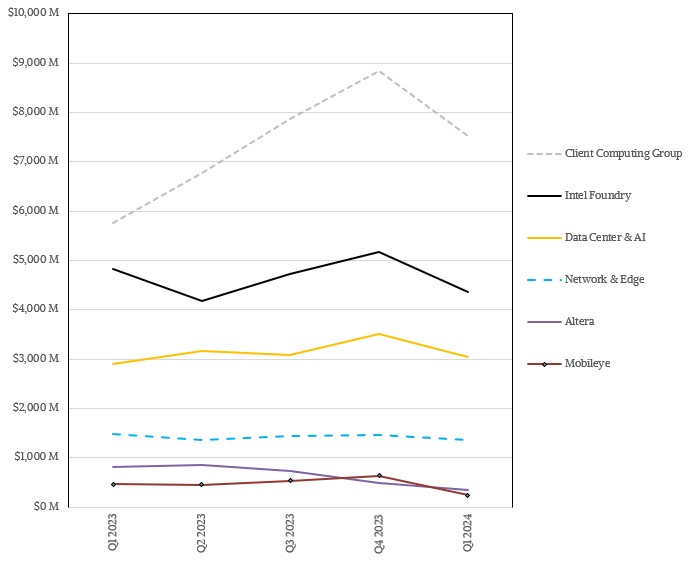

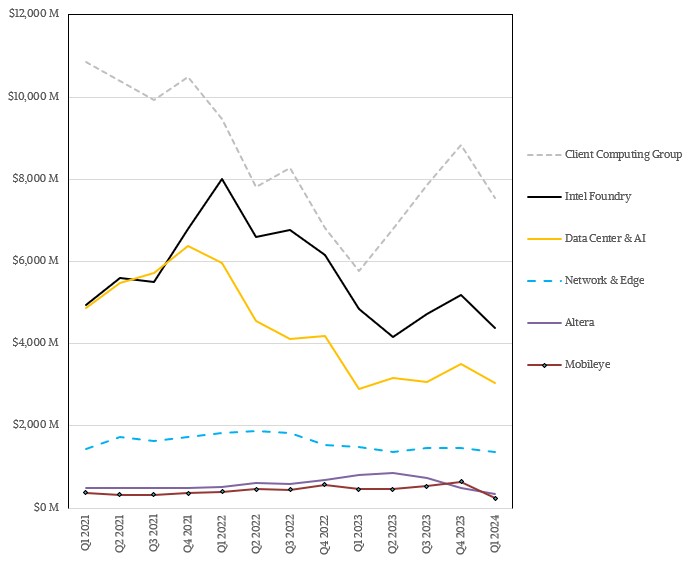

For those of you who think visually, here is a chart that shows the important groups and how their revenues have fared:

We find this chart to be almost useless. You cannot get a feel of the ups and downs of these businesses from such a small amount of data. Intel should have given us three years of data plus the current quarter, or even a decade of data plus the current quarter, so we could fully understand what has happened.

The good news is, Intel gave us a good sense of how Intel Foundry fared for the past three years in its annual data, and we know exactly how well and poorly the Altera business did. So we can extract the Altera business out of the numbers we had for the DCAI and NEX groups to recast the data back to Q1 2021 when Pat Gelsinger, Intel’s first chief technology officer and formerly the general manager of its Data Center Group, returned to the company after running a chunk of EMC and VMware as its savior chief executive officer.

This may all be painful, but Gelsinger is doing the right things and is a tireless cheerleader for the future of the chip company that he loves and that without question he should have been running all along.

In any event, we got out that trusty Excel spreadsheet and projected what Intel Foundry revenues would have been for the eight quarters of 2021 and 2022 and extracted Altera out of the other groups, and if you do this, then you actually get something that shows you something. Take a gander:

Intel’s inability to get 10 nanometer, 7 nanometer, and 5 nanometer processes in the field at roughly the same time that TSMC did hurt its product designs and left the door open for AMD and the Arm collective to get into the datacenter. The lack of a GPU alternative to Nvidia has also harmed Intel and the industry. Imagine a world where Nvidia had to open up its software and interconnect specifications because users could demand this?

This chart also shows you why Intel has been banging the drum so hard about Intel Foundry. The foundry business is its second-largest group, and probably will remain so for many years unless something weird happens in the IT sector. OK, something even weirder. After Gelsinger left, Intel operated as a monopoly supplier of CPUs in a world that loved CPUs, and it did not keep its foot on the gas for its foundry innovation. And the lack of CPU competition from AMD and the Arm collective allowed it to get away with it for many years, raking in big bucks and having operating margins around 50 percent even with the extra heavy burden of the costs of that foundry business on its back.

But that competition came, as it always does, and suddenly Intel was not a low-cost producer of server CPUs or even a producer of much-wanted GPUs.

With all of that in mind, let’s go over the Intel numbers for the first quarter ended in March and take a look out into the future.

In Q1, Intel’s revenues were up 8.6 percent to $12.72 billion, but it posed a net loss of $381 million. That was a lot better than the $2.76 billion loss it had in the year ago period, when revenues were only $11.72 billion, but the company also burned $3.72 billion in cash, with its cash and marketable securities standing at $21.31 billion as the quarter ended. That is not a lot for an Intel that is eager to build foundries and invest in chip designs, which is why getting $45 billion of cash, loans, and tax incentives as part of the CHIPS Act was crucial to the survival and revival of Intel.

In the quarter, the DCAI group had sales of $3.04 billion, up 4.7 percent, with an operating income of $482 million, up by a factor of 21.9X from the abysmal $22 million operating income DCAI posted in the year ago period. (But hey, this was an actual loss before Intel Foundry was created and started shouldering the losses that were rightfully its own.) The “Sierra Forest” Xeon 6 E-core chip is imminent and is etched with the Intel 3 5 nanometer process, and the “Granite Rapids” Xeon 6 P-core chip will be released in the third quarter of this year using the same Intel 3 process. (We profiled these chips last fall.) The “Clearwater Forest” Xeon 7 E-core, using Intel’s 18A process, is on deck for next year.

“We continue to expect share trends to stabilize this year before improving in 2025,” Gelsinger said on a call with Wall Street analysts. “While budgets are still being prioritized to generative AI build-out where we have a strong position in the head node, customer conversations continue to show improving signs for traditional CPU refresh starting in late Q2 and into the second-half.”

Interestingly, Gelsinger said that Intel now expected more than $500 million in revenues in the second half of this year for its Gaudi 3 matrix math accelerators, which were launched two weeks ago and which are absolutely competitive with Nvidia’s “Hopper” GPU accelerators for AI workloads – especially Llama models running atop the PyTorch framework. Back in October, Intel said it had a $2 billion pipeline for Gaudi compute engines, so with only $500 million of that being converted, that means Intel is supply constrained on TSMC’s 5 nanometer process, which is used to etch the Gaudi 3.

“We are three years into our transformation and 2024 represents the steepest part of the climb with five node in four year start-up costs peaking and the majority of our volume on pre-EUV process nodes with uncompetitive economics,” explained Dave Zinsner, chief financial officer at Intel. “However, as we the crest the hill and look toward the next few years, we have strong wins at our back and a clear path to achieving the mid and long-term financial targets we laid out earlier this month.”

Altera and NEX are both dealing with inventory capacity issues that are being burnt off, and their revenues and operating income are obviously looking pretty weak. But Gelsinger said on the call that they would start turning around in the second half along with the CPU business. Average selling prices of Xeon CPUs are already on the rise thanks the existing Xeons, and this trend is expected as Intel delivers CPUs on advanced processes and with a competitive number of cores and features. Intel is standing by its prediction that Altera will break $2 billion in sales for 2024.

Server Spending Holds Up Despite Every Damned Thing

Our increasingly networked and compute-intensive lives are driving the server business, and despite the cornucopia of fear, uncertainty, and doubt that spans the globe, the appetite for compute as expressed in shiny racks of servers or metal pizza boxes or an occasional tower sitting in a closet or under a …

Prime Contracting No Longer One Of Intel’s HPC Aspirations

Intel has spent the past nine months reorganizing itself in the wake of Pat Gelsinger becoming its chief executive officer in January, including new groups and divisions and new managers for them that were revealed in June. But the fate of its HPC organization, which has been less focused than …

It’s All Uphill From Here For Intel’s Datacenter Business

Intel’s Data Center Group has just turned in the third best revenue quarter in its history, just behind the two thirteen-week periods that started off 2020, which was before the coronavirus pandemic had hit and just after it hit and the full effects were not seen as yet. Oh, and …

“Imagine a world where Nvidia had to open up its software and interconnect specifications because users could demand this?”

Exactly! In this cut-throat business, such events (unfortunately) often suggest that one’s erred awfully close to the precipice, Sun Microsystem-style … and even an exceptionally able Jonathan Schwartz open-sourcing Solaris, and ZFS, and what have you, may not suffice to quell the now overwhelming call from the void …

But Gelsinger’s doing a great job steering Intel away from the cliff in my estimation. Bringing Aurora up to full speed, and executing right on Granite Rapids, should do wonders for confidence (to me)!

So, when is Aurora going to be full speed? Is it already beyond the cut-off data for the 2024 Top 500 submissions?

“Submission deadline for the June release of the TOP500 List is April 28th (23:59 PST). All system reported have to be installed and submitted by April 19th.”

Exactly! We’ll know for sure within 2 weeks, in Hamburg ( https://www.isc-hpc.com/ ), but my hope is that they’ve updated the software to get 70% or better efficicency, and installed (or powered-up) the other half of the CPUs and accelerators, which should give the machine at least 1.5 EF/s on HPL.

Foundry is code for brittle labor business, it can be moved easily. Let’s keep in mind Intel had the Microsoft cloud blade for many generations at full IDM IP, likely $500 each with full IP. They had VR11HC, then 12, then 13, then 14….wait for it…now comes 10nm Icelake debacle. They forced Microsoft to design their own chip now they have job shop labor at $29.00 and no IP…