With new generations of GPUs and other kinds of AI accelerators either shipping or soon to start shipping and new CPUs also soon to be available from Intel and AMD, and sales already at a historical high level at Supermicro, you might not be expecting for sales to bust through a whole new higher ceiling starting in the next quarter. But that, apparently, is what Supermicro thinks will happen.

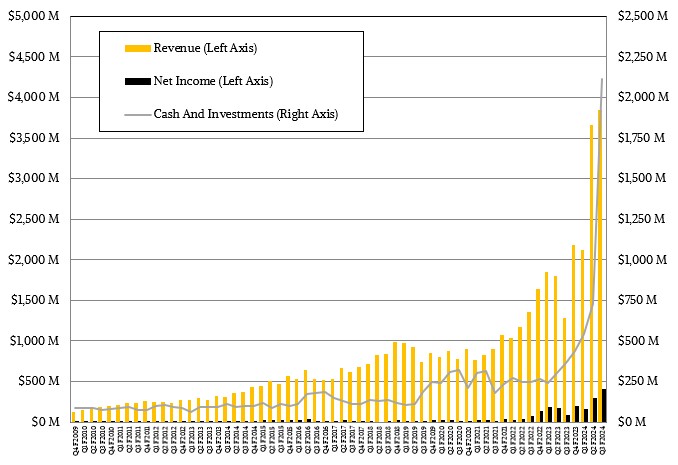

In the quarter ended in March, Supermicro had revenues of $3.85 billion, down a smidgen from Wall Street expectations but in the dead center of the range it told Wall Street to expect and a factor of 3X higher than in the year ago period. Charles Liang, co-founder and chief executive officer at Supermicro, said on the call with Wall Street analysts that were it not for some key component shortages, it could have pushed revenues even higher. Interestingly, Supermicro projects that in its fourth quarter of fiscal 2024, which will end in June, it would have sales of between $5.1 billion and $5.5 billion, which will represent a factor of 2.3X to 2.4X increase compared to the year ago period.

This is phenomenal growth by any measure, and relatively unheard of in the server market. But when Wall Street is disappointed, it lets some of the air out of a company’s market capitalization. That certainly happened to Supermicro this week, and has been happening, in fact, since the middle of March, when Supermicro had an amazing $69.6 billion market capitalization. It stands at $44.7 billion as we go to press, which is a decline of 35.8 percent. But then again, the company’s stock is up by a factor of 2.7X in the past year, a reflection of the explosive growth Supermicro has seen, particularly in selling clusters of rackscale systems aimed at AI workloads.

In the quarter, thanks in part to some tax benefits but mostly thanks to higher server volumes, Supermicro was able to bring $402 million to the bottom line, a factor of 4.7X increase over Q3 of fiscal 2023, and representing 10.5 percent of revenues. This sets a new profitability high water mark for Supermicro. And we have been complaining, on behalf of all system OEMs, that the chip makers have to give them more margin so they will be in business into the future, and this seems to be happening here.

And thanks to its many quarters of increasing profits and a float of 2 million shares, the company exited the quarter with $2.12 billion in cash and equivalents, a war chest that allows it to pay for allocations of CPUs and GPUs upfront and become less dependent on the direct allocations of compute engines of its largest hyperscaler and cloud builder customers. Meta Platforms is a big one, and we think Supermicro is also making machines for Nvidia, too. And very likely GPU cloud upstarts CoreWeave and Lambda, too.

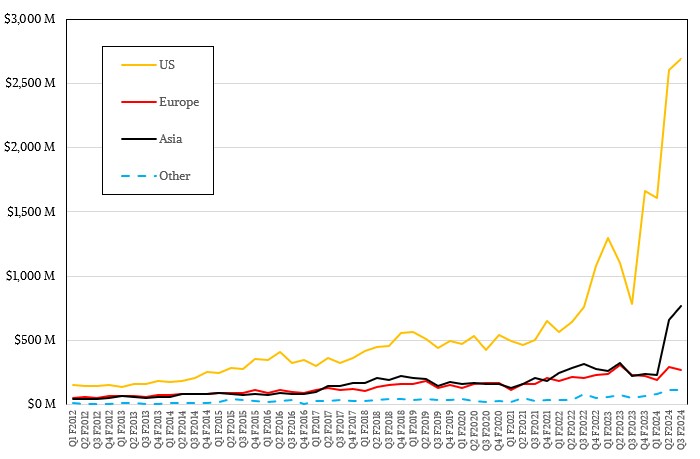

We think these companies and other companies have a strong desire to buy machinery manufactured close by and within their region when they are sold in North America, Europe, and Asia outside of China and it is a serious political and supply chain risk to make iron in China. And Supermicro is absolutely benefitting from this.

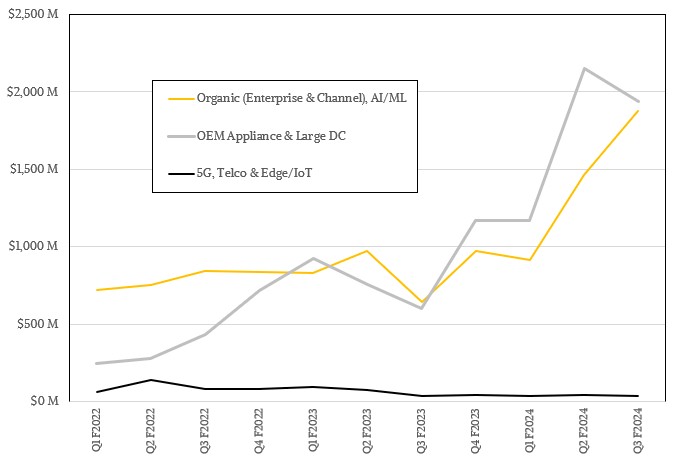

Supermicro is also benefitting from the desire to buy and deploy at rackscale. On a conference call with Wall Street analysts, Liang said that between April and June, the company was building rackscale AI clusters – what it calls SuperClusters – for three customers that together comprise over 1,000 racks of iron.

These machines for three big customers are based on Nvidia “Hopper” H100 and H200 and “Blackwell” B200 GPU accelerators, and at 64 GPUs per rack, that is more than 64,000 GPUs. The Nvidia GPUs all by themselves cost in the range of $2.25 billion for these machines if you assume an average price of $35,000 a pop, which is reasonable if you think these machines are skewing towards H200s and B200s proportionately, and that implies that these three clusters might have a total price of $3.5 billion to $4.5 billion, depending on how they are configured with CPUs, memory, storage, and networking.

All three customers are buying direct liquid cooling (DLC) from Supermicro, which builds it own cold plates for components and its own chilling towers as part of a “total solution” package that both Supermicro and Nvidia like to talk about in precisely that manner. The SuperCluster racks are rated at 100 kilowatts, which is a factor of 7.7X higher than the typical infrastructure rack at a high-end enterprise, which averages around 13 kilowatts.

These deals, which call for shipment in the fourth fiscal quarter, are why Supermicro has such strong visibility into that quarter and why it can confidently raise its guidance for fiscal 2024 revenues. Supermicro now says that it will have a top line of between $14.7 billion to $15.1 billion. That is $14.9 billion at the midpoint of guidance, which represents a factor of 2.1X growth over fiscal 2023.

If Wall Street is disappointed with Supermicro, that just shows that maybe Wall Street should not have been so exuberant in the immediate past because the company is doing better now than when its market cap was a third higher a few months ago. This is what happens when stock value is only loosely coupled with business performance and tightly coupled to the sentiment of people who don’t know the business and who therefore have unreasonable expectations.

With HPC Humming Along, HPE Awaits Its AI Boom

The ProLiant server business is down in the dumps, and the storage business is in a slump. But petascale and exascale supercomputer deals based the combination of AMD CPUs and GPUs have filled in a lot of the gap. And Hewlett Packard Enterprise is now waiting, like all OEMs and …

Deutsche Bank Tag Teams With Nvidia On Financial Services AI

In many industries, embracing AI in the application software stack it is not just a matter of training some large language models or recommender systems against general and then specific datasets and plugging it in. And in any regulated industry – particularly financial services because it deals with Other People’s …

How Long Before AI Servers Take Over The Market?

When hyperscalers and cloud builders think about their infrastructure, they talk about megawatts and they think about the mix of serving and storage and the total capacity that is delivered in a megawatt of power. And of course they also think in terms of budgets because money is, in fact, …

Wow! That’s a more than 5x growth in US revenues since Q3 2021, and now sustained over 2 consecutive quarters (Q2-Q3 F24). Great results for that company with a most enthusiastic, dynamic, optimistic, and approachable of CEOs, and contagious “can-do-attitude” (IMHO)! ( https://www.nextplatform.com/2023/09/28/supermicro-at-30-from-designing-ai-chips-to-selling-ai-systems/ )